5 Reasons to Talk About Harris’ Medicare Home Care Benefit – Center for Retirement Research

Long-term care screening is good for all of us.

As someone trying to become more knowledgeable about long-term care, I was surprised and intrigued by Vice President Harris’ proposal to create a new home care benefit for Medicare beneficiaries. The details of the program are still unclear, but it sounds like:

- It may be available to Medicare beneficiaries who need help with basic activities of daily living such as bathing, eating, and toileting or who have a severe cognitive impairment such as Alzheimer’s disease.

- It would include an average of 20 hours of paid care per week (based on the statement in the campaign’s fact sheet that “the majority of seniors with long-term care needs can still live in their own homes with an average of 20 hours or less per week of care”).

- It would cover the full cost of low-income earners “with a sliding scale of cost-sharing for high-income seniors.”

Although I had somehow concluded that the most important thing was some form of social insurance for those who run into catastrophic long-term care costs, I am glad to have a discussion about the new Medicare home care benefit for five reasons.

First, for long-term workers and retirees, the possibility of needing care later in life is a real concern. Many think that it is the worst case scenario – that they will need intensive care for a long time. Fear of dependency makes retirees reluctant to use their 401(k) balances, depriving themselves of needs as they age. The debate about the limited benefit of Medicare home care may clarify that not everyone gets dementia.

Second, to the extent that people expect long-term care support from public programs, they are already mistakenly thinking of Medicare as the primary provider. In fact, Medicare does not cover long-term care services. Another source of confusion may be that Medicare covers up to 100 days of care in a skilled nursing facility, after a hospital stay of at least three days. Similarly, Medicare also covers certain homes health care services for up to 21 days and provides hospice care. But most care covered by Medicare is medical, temporary, and related to a serious or life-threatening event. The debate over increasing the home care benefit may help clarify the limited role Medicare plays in long-term care.

Third, Medicaid — not Medicare — is the primary payer for long-term care. But the program – which has strict income and asset tests – is complicated by provision rules that vary by state, home care services provided by state discretion, and different definitions of “limited” financial resources. In addition, approximately 700,000 people are on the waiting list for some types of home care services because more people want these services than the states can accommodate, due to a lack of both funding and service providers. The debate over the Medicare home care benefit may shed light on the complexities and limitations of Medicaid.

Fourth, the most important conclusion that can emerge from the Medicaid audit is that the middle class has no protection. The wealthy can afford insurance and – despite the program’s difficulties and limitations – those with limited income can get some help from Medicaid. Middle-class families, however, must rely on their resources and the costs they face are staggering (see Figure 1). The debate over the new Medicare home care benefit may focus on the costs for families dealing with intensive, long-term care.

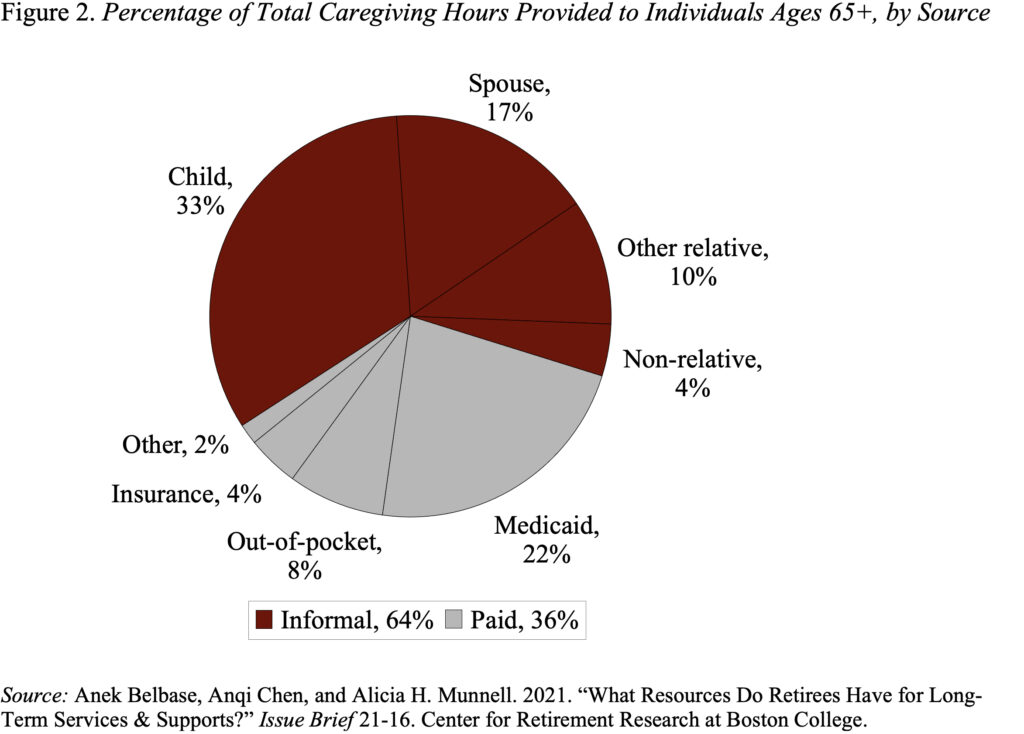

Finally, although Medicaid is the largest payer of paid care, it only covers 22 percent of the hours needed to care for those age 65+ over their lifetime (see Figure 2). A common source of support is informal unpaid care provided by family members – especially spouses and children. This caregiving places a heavy physical, emotional, and financial burden on caregivers. The debate over the Medicare home care benefit can help highlight the burden borne by unpaid caregivers.

The bottom line is that the Vice President’s proposal shines a bright light on a serious problem. If legislation were to be enacted, many decisions would have to be made about who is eligible, the relationship to other Medicare benefits, the relationship to Medicaid benefits, and how costs will be covered. I also hope that the debate includes some discussion about whether long-term care services should be up to first dollar payment for everyone as opposed to creating a system that includes dangerous costs. My gut is that most families can cope with a year or less of low to moderate care; the people who really need help are those facing years of intensive care due to dementia or other long-term debilitating conditions. In any case, a serious discussion of the issue of long-term care would be good for all of us.

Source link