A recent report from CoreLogic revealed that “piggybacked mortgages” for FHA borrowers reached a new high in June of this year.

Although piggybacked home purchases have historically been higher for those taking out FHA loans, they have increased in recent years.

The culprit is probably high housing prices, which has made it very difficult to come up with low down payments, even if you only need 3.5%.

For reference, a piggyback loan is a second loan that is taken out simultaneously with the first mortgage to extend the total amount of money.

An example would be a first mortgage for 96.5% of the purchase price and a second piggyback on the remaining 3.5%.

While this is helpful for homebuyers who don’t mind down payment and closing costs, it can present problems if they are also trying to renovate or sell.

FHA Piggyback Share Goes Up to 18% on Home Loans

From June 2022 to June 2024, the share of FHA purchase loans backed by hogs increased from 10.8% to 18%, according to CoreLogic.

That’s nearly double the 9.8% share seen back in 2017 when the housing market seemed to normal.

And while FHA loans tend to have a higher piggyback rate in general, the latest increase is 67%.

It shows how home buyers have expanded recently, especially those who need an FHA loan to qualify.

FHA loans tend to go to low-income home buyers and/or those with low credit scores as you can get a 3.5% loan with a minimum 580 FICO score.

Currently, you need a minimum 620 FICO score to qualify for a personal loan backed by Fannie Mae or Freddie Mac.

CoreLogic notes that ongoing affordability issues have disproportionately impacted low- to moderate-income homebuyers because these piggyback loans are often seen in low-income neighborhoods.

The median property value of homes purchased with an FHA piggyback loan was $34,600 ($168,600 vs. $203,200) in 2017.

This gap increased to $55,000 ($237,800 compared to $292,800) in June 2022 to $64,000 ($255,000 compared to $319,000) in June 2024.

So arguably the high-risk pool is overextended, at least in terms of loan-to-value (LTV) ratio.

Many FHA loans with Piggybacks are already underwater

Remember the underwater mortgage? I haven’t written about them in what feels like a decade, but they’re starting to make a comeback.

All of this has to do with rising home prices and low or no down payments, combined with the recent softening of the housing market.

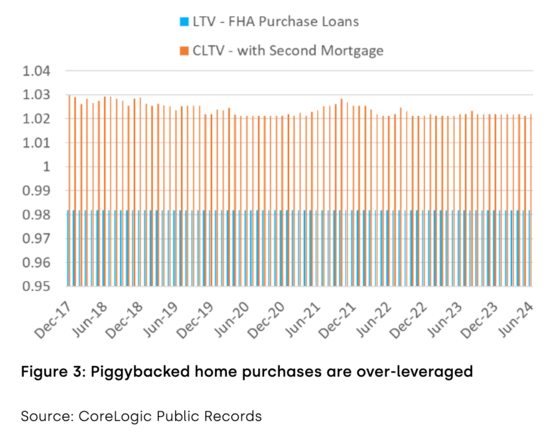

And the fact that right out of the gate, the average origination LTV for FHA mortgage loans is 98.19%.

That’s before the second mortgage is considered, which puts the combined LTV, or CLTV, at 102.2%.

Although it is not a concern if the borrower cannot make their monthly payments, it becomes a problem if they cannot.

For example, if the economy takes a downturn and/or the borrower loses his job, he has zero skin in the game. And maybe a little reason to stick around…

This can be even worse if property prices fall as well. While house prices are still expected to rise slightly at the national level, individual markets across the country are now under pressure.

If the borrower is underwater, there is a high chance that he will default. In addition, it can make it more difficult to qualify for refinancing to take advantage of lower loan rates.

Technically, FHA borrowers are maxed out at 125% LTV on streamline refis if they have a second mortgage. And the existence of a second loan makes the process, well, a little more organized.

So borrowers who desperately need help paying off can be locked out unless they hold a second piggyback mortgage that puts them underwater. It can be even more difficult to sell the property.

While not yet a problem, things can change quickly if the economy falls into recession and/or housing prices begin to decline.

Before creating this site, I worked as an account manager for a real estate broker in Los Angeles. My experiences in the early 2000s inspired me to start writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the mortgage process. Follow me on Twitter for the latest.

Source link

.png?w=390&resize=390,220&ssl=1 "Introduction: Why Commercial Lending Will Look Different Towards 2026")