Why do house prices keep going up as house prices go up? A number of people predicted that house prices would drop significantly as mortgage rates increased, but that is not what happened.

This is not a new idea – I have been dealing with people predicting the housing crash since 2012. Doom porn is a fad in America and is often made by haters. The Federal Reserve. But today, I’m going to use data to explain why, even in 2024 — the third-lowest calendar year for home sales on record (adjusting for labor) — national home prices didn’t drop.

Here are the reasons given for why house prices have been said to be falling for the last 13 years:

Folks, these are not real estate experts or analysts. I have a rule: don’t listen to anyone online unless they have their name, face, written 2024 price forecast, five year home price forecast, and working model.

So, why haven’t home prices come down with high mortgage rates this year?

However, if history is our guide, housing prices have rarely fallen in general since 1942. If you take 2007-2011 out of the equation, we only had one negative year; that was 1990, and that was a 1% drop.

When you ask housing crash addicts why home price forecasts don’t work, they usually say we have to adjust home prices to inflation, gold prices, or some other silly historical indicator that doesn’t work in today’s economy. This group is just a cult, and their X accounts have been wrong for the past 13 years.

Let’s take a look at today’s home sales report to see if you can explain why home prices haven’t fallen year over year. In order to experience a real price crash, we would have to see an increase in housing prices and distressed sellers. As you’ll see below, inventory is growing, but it’s been a quiet, healthy increase through 2024, not a flood of homes coming onto the market.

I National Association of Realtors‘ The current home sales report shows home sales fell just 1.0% from August to a seasonally adjusted annual average of 3.84 million in September. Year over year, sales were down 3.5%.

“Home sales have slowed by nearly four million over the past 12 months, but factors typically associated with high-end home purchases are improving,” said NAR senior economist Lawrence Yun. “There are more choices for consumers, mortgage rates are lower than last year, and the continued addition of jobs to the economy. “Maybe some buyers are hesitant to go ahead with big expenses like buying a house before the next election.”

Where I disagree with Yun is this: We have more inventory because demand is soft, and we have more new listings this year compared to last. If mortgage rates were below 5.75% – 6.25% this year, we would be increasing home sales regardless of inventory data. Inventory is growing, and home price growth is slowing from an unhealthy housing market in 2021 and early 2022, but not enough to lower home prices nationally.

Below are the charts from today’s report. Note: Median sales price data is seasonal. Many people will try to trick you into thinking that house prices fall in the second half of the year, but this is just a normal seasonal price drop.

Using NAR data, the average amount of active inventory since 1982 has been between 2 and 2.5 million. In 2007, the active number increased to 4 million. Today, it is only 1.39 million. With monthly housing supplies in over four months and approaching my target of 1.52-1.93 million in active inventory, the housing market is flat. We have some equipment to buy homes—we don’t need it because mortgage rates are so high.

That’s fine, but you might ask: If prices follow volume, why haven’t national housing prices seen a big drop? Well, you would need to add distressed sellers to the mix, as we saw from 2007 to 2011, and we don’t have that in the data now.

Consumption rates are historically low

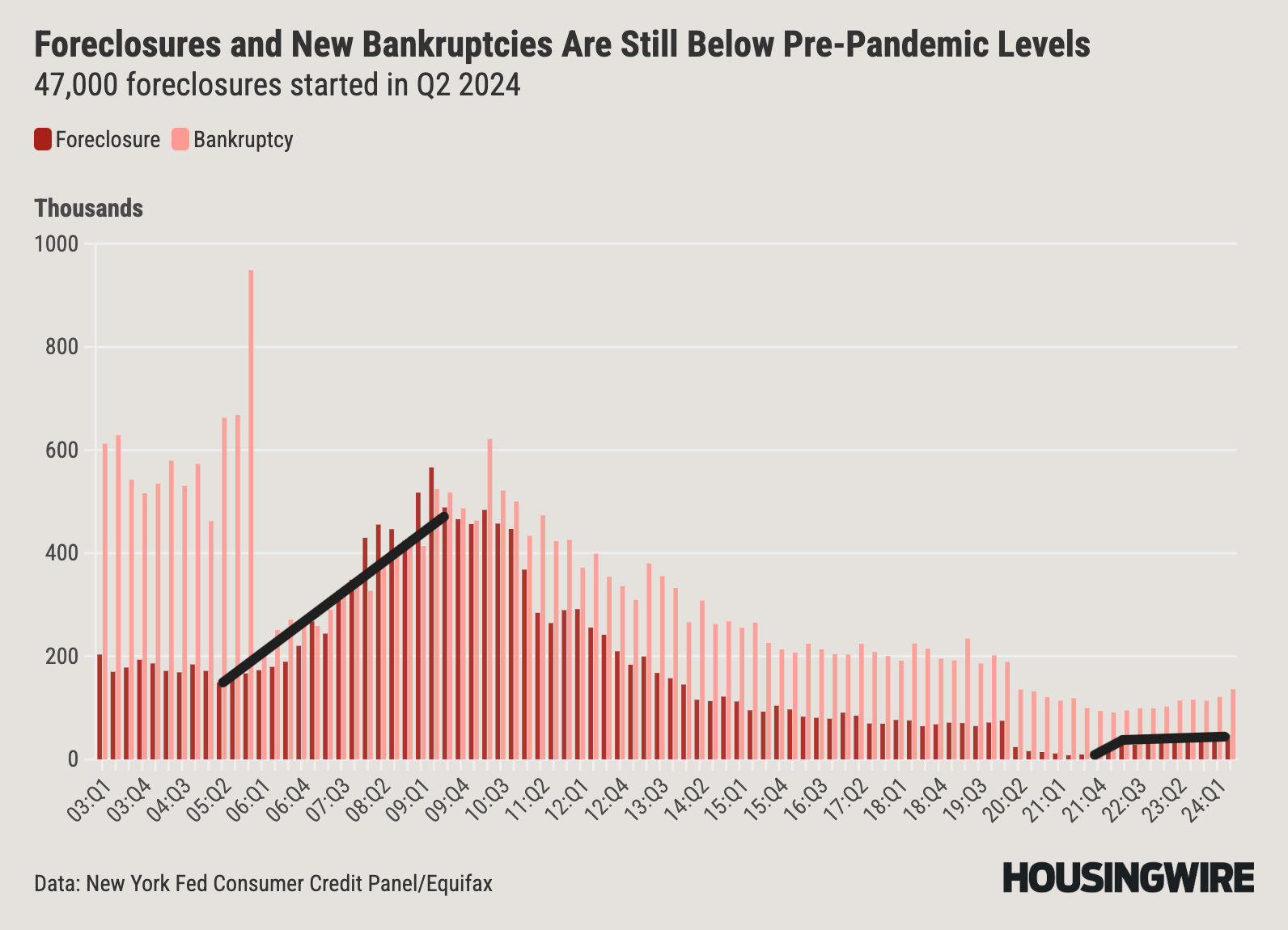

As you can see below, the data for foreclosures and bankruptcies increased between 2005 and 2008, all before the recession of job losses began. Today, closures have not even returned to pre-COVID-19 levels.

No major forced sales are taking place

Below is our data on new listings, which shows that 2023 and 2024 will be the lowest listing periods ever. This data was trending between 30,000 and 90,000 weekly five years ago. Compare that to 2009 to 2011, where this data line is active 250,000 to 400,000 per week. That’s a big difference folks. It is the only time in more than 80 years that the national home values crashed while the new listing data is running at three times what we have seen in the last few years.

Tons of equity in this one

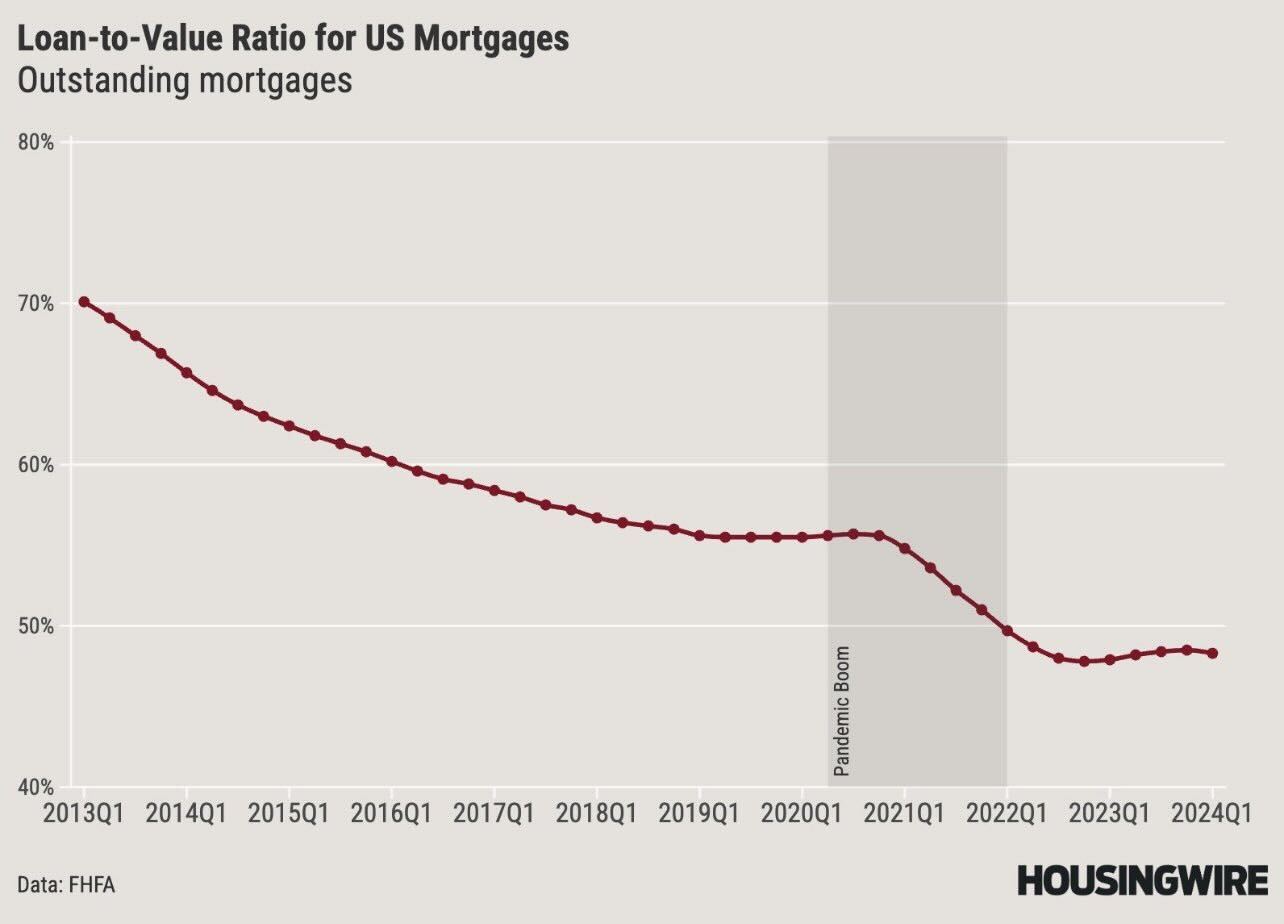

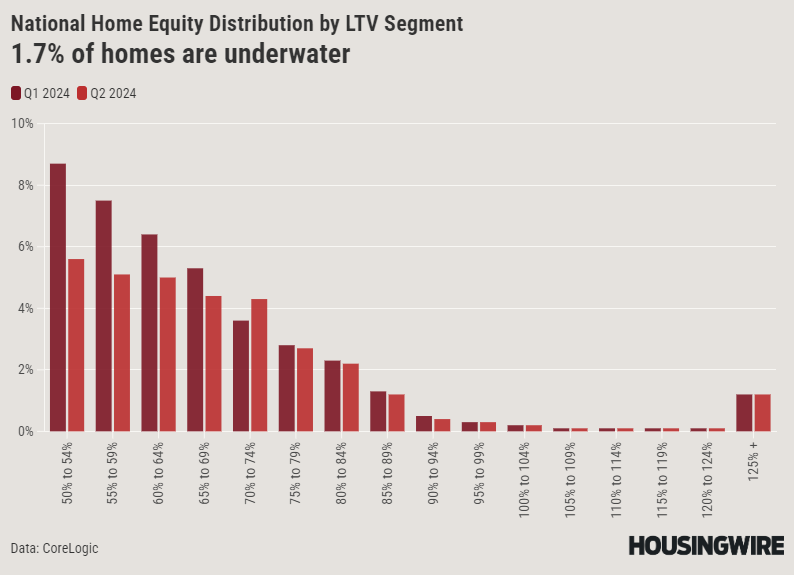

Today, few people sell their houses underwater; the percentage of houses under water is 1.7%. In addition, the loan-to-value of mortgage-backed homes is less than 50%, and more than 40% of homes in America don’t even have a mortgage. In 2010, when the new listing data broke, more than 23% of homes in America were underwater.

I want to keep things simple: We’ve had one period where national housing prices went down, and to replicate that model, you’d need the same variables, mostly distressed sellers or people forced to sell in a declining market. Some people believe that the rise in mortgage rates over the past two years could mean that house prices will automatically fall. History contradicts this assertion. Data has shown for decades that we have had periods in history where we have had both rising mortgage and asset prices without housing price crashes.

As we can see in today’s home sales report, home sales have declined though they are unbreakable. I discussed this on the HousingWire Daily podcast last year, explaining my housing economics model. For a home price crash to happen, you need a bad economy, depressed big sellers, and no government aid to help American citizens, which means you need a repeat of the Great Recession of 2008. The above data shows that this is not the case today.

Related

Source link