Over 5 years, Scottish Mortgage made 2,475% on Nvidia but lost 83% on this FTSE growth stock.

Image source: Getty Images

Scottish Mortgage Investment Trust (LSE: SMT) prides itself on finding the next high-achieving growth stock. But this approach comes with an equal amount of flexibility.

For proof, look at Scottish Mortgage’s share price, which has risen 41% in the past 18 months but remains 37% below its 2021 peak.

When the S&P 500 again Nasdaq both are climbing to new highs almost daily, which has frustrated many shareholders (myself included).

Granular data

Perhaps that is why there has been a visible effort by management to increase cooperation with shareholders. More interviews, webinars, updates, information, that kind of thing.

There was even an October lunchtime interview with lead manager Tom Slater at The Timeswhere we learned that he likes eggplant involtini and uses a smart mattress to track his sleep.

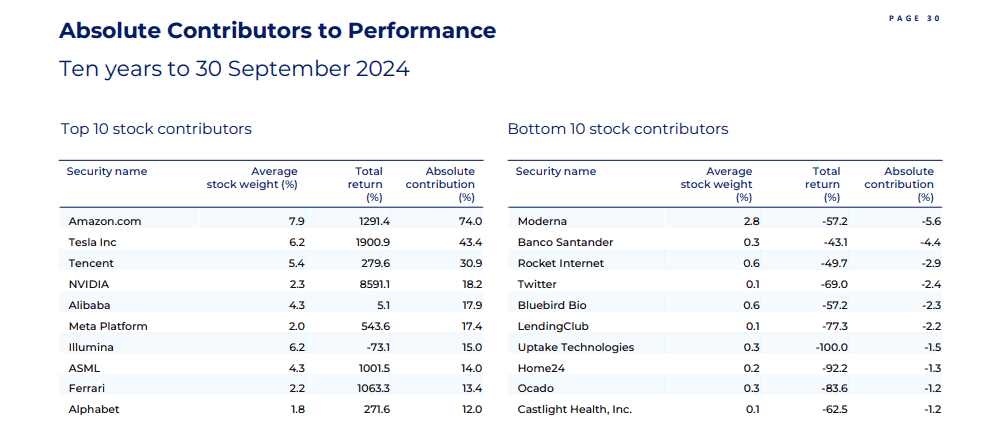

Recently, Scottish Mortgage also released its quarterly data package, which gave shareholders a peak under the bonnet on portfolio returns. There was some interesting information there, I think, that proves the power of long-term investing.

The FTSE Flop

Only 3% of the trust’s assets are currently in UK shares. One of them Ocado (LSE: OCDO), an online grocery/bot company.

According to the Q3 data pack, the trust’s investment in it fell by 83.6% in the five years to 30 September. Wow.

With the benefit of hindsight, we realize that investing in Ocado in 2020 at the height of the pandemic-driven online grocery boom was foolish. It’s been downhill ever since, with post-Covid conditions normalising, and Ocado’s growth rates.

The company has been downgraded even to a blue-chip FTSE 100 after its dramatic fall. The problem comes down to profit, or lack thereof. In H1 2024, it reported a pre-tax loss of £154m.

I had a brief encounter with the stock last year, opening a small position and then running for the hills when the CFO said it would be another “six years” (!) before the company is expected to do a before-tax benefit.

Another risk here is that Ocado needs to tap shareholders for more money at some point. After all, the high-tech robotic warehouses that we build in partnership with the world’s leading buyers don’t come cheap.

That said, Ocado has been the UK’s fastest-growing grocer in recent months, and its robotics business still has exciting potential. However, I won’t be investing, preferring to get exposure to the Scottish Mortgage stake (what’s left of it).

Asymmetry works

With every few Ocados down 80%+, trust hit the jackpot with the big winner.

We saw this in the data packet, which confirmed that it is affected Nvidia again Tesla returned 2,475% and 1,415%, respectively, over five years. Good.

Within 10 years, the asymmetric return was even more pronounced. The trust was sitting on five ’10-baggers’ (10x returns). These were Nvidia (actually an 85-bagger!), Tesla, Amazon, ASMLagain Ferrari.

It is these companies that have helped Scottish Mortgage deliver a return of 347% over the past decade, beating the 211% produced by FTSE Worldwide index.

The danger is that managers fail to identify the next generation of stock market winners. But when I look at the portfolio today, I am positive that they are in there somewhere, ready to develop more benefits.

Source link