A good reminder that the lenders are always quick to raise their cooperation prices

I keep hearing that lower prices are in partnership with the world’s trading warehouse.

That despite the stock market and maybe high quality values due to tax rates, minimum maximum prices.

But how far is it really down? And in what expense? And do you actually bite, except for recent home consumers who want to Reful?

While nothing is wrong with looking at something good during these challenges, it should be noted that the amounts are no longer within 7%.

In fact, in some way, 30 to 6.75 years were organized today!

Borrowed tax prices return to 7%

While last week and the changes were good at masked prices, today did not do so well.

As I pointed out for a few days, the great dealings of the mortgage such as those we see recently is suspended in their tracks without warning.

Note the rate of the mortgage I said, and that is exactly what we have today.

Two appointed, who had collapsed from 7.25% in mid-January to 6.60% on Friday, returning to 6.75%.

It seems to be set to fall, it is possible to beat 6.50% in the next, but the prices jump back today, despite the wrong day in the stock market.

Perhaps the bonds still receive in the stock market, very variable yet.

Perhaps the bonds need soul while trying to determine the next movement of President Trump.

But Takeaway here is the prices of a high-quality asset (0.25%) away from 7%, at least according to MND.

So maybe that silver lump is not so much.

After enjoying a fun custom in the bottom, the mortgage rates seem to find anywhere.

Did you know that they are actually too low as it later in October of the past year?

While your memory can fail, they were. The 30-year planning is basically 6%.

Of course, the prices are lower than the back of the past, which can raise home sales in this spring, but they stay close to 7% than 6%.

And days like this make you wonder if we can also visit those standards again, no doubt they will produce air from the most fragile housing market.

Currency lenders are borrowing will use any excuses for lifting up to the pricing

The lesson today is that Printing Finance Lenders will use any excuses to expand prices.

Why? Because it is very easy to play protecting, especially in unsure places. They don’t want to be caught in the wrong side of trade.

Remember, they donated the limited interest rates for next 30 years. They get what is wrong and can be a costly mistake.

As a result, the lenders will take their time to reduce prices, but if they even find the accident and they will raise it immediately.

With MND by MND, 30 repairs jump from 6.60% on Friday 6.75% today. That is one single day’s departure of their daily survey.

Granted, 30 years began at 12 BPS on Thursday, followed by an additional 3-BP on Friday, together 15 BPS.

So the complete improvement of last week was removed in one day.

That is how it goes. You must release a few days to win to improve, but one day you can restore completely.

They are two steps forward, with one big step back.

But wait, there is a chance this is not just bounce

Before I drink a lot here and I offer the latest assembly of borrowed material, I should be careful that this can only be bounce.

Stock market does this all the time. After a few days later, there is a meeting. Basically the soul.

Stocks and levels of loans do not go with a straight line up or down, especially after the great meeting in one place.

That would be what we see today. Admittedly, at present both stocks and bottles of bond are low, unusual.

Usually, when shares fall, there is a delivery of bonds, which increases their price and reduces their crop (interest rate).

Not so right now. Everything is sold as Trump is threatening many tax values.

It is as if no one knew what to think, and there is no safe, even government obligations that are often a safe place for investors.

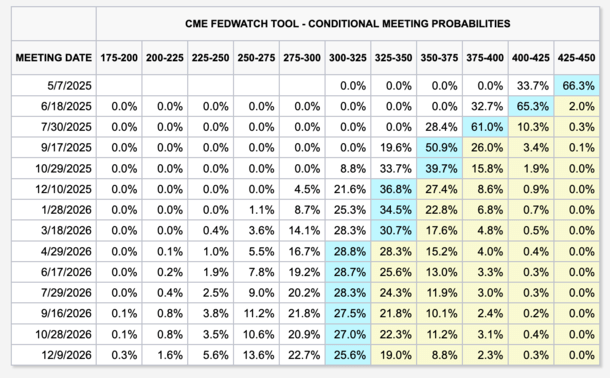

But when we bring us closer, here is something to consider. The Fed is now looking to cut its Federal Funds estimates four times in December, with the Fedhthath.

And while the Fed now, the bonds take directions from the Fed, and if the discrepancy is expected, and you may see the heat of bonds 10.

That often translates the highest amounts of mortgage support.

So now it may be the best time to take a long view instead of being caught in daily madness.

It is no easy if you have to lock or float the levels of money in the next few days or weeks, but it is confirmed if you want to end the encodes. Or maybe buy a home.

Learn to: How to track the tax rates easily.

Before creating this site, I worked as an account official because of the seller of the sales asset in Los Angeles. My first experience of 2000s encouraged me to start writing about 19 years ago to help the consumers that would be better and better. Follow me on X by taking hot.

Source link

.png?w=390&resize=390,220&ssl=1 "Introduction: Why Commercial Lending Will Look Different Towards 2026")