Mortgage Q&A: “Are mortgage payments going up?”

While this sounds like a silly question, it’s actually a lot more complicated than it seems.

You see, There are many different reasons why a mortgage payment can go upwith no apparent interest rate change. But let’s start with that one and go from there.

And yes, even if you have a fixed rate mortgage your monthly payment can go up! You’re not out of the woods yet.

While that may sound like bad news, it’s good to know what’s coming so you can prepare accordingly.

Mortgage Payments Can Increase With Interest Rate Adjustments

- If you have an ARM your monthly payment can go up or down

- This can happen every time it repairs, be it every six months or a year

- To avoid this payment surprise, simply choose a fixed rate mortgage instead

- FRMs are actually priced much closer to ARMs anyway so it may be to your advantage to stick with a 15- or 30-year fixed term.

Here’s a simple one. If you have an adjustable rate loan, your loan rate has the ability to adjust either up or down, as determined by the interest rate.

It can go up or down when it becomes fixable, which happens after the first time of the teaser rate ends.

These rate changes can also occur periodically (annually or biannually), and throughout the life of the loan (with a certain upper number, such as 5% up or down).

For example, if you take out a 5/1 ARM, the first adjustment will occur after 60 months.

At that time, it can increase significantly according to the existing caps, which may be 1-2% higher than the initial level.

So if your ARM started at 3%, it may jump to 5% on its first adjustment. Or more!

For a $300,000 mortgage, we’re talking about an increase in monthly payments of about $350. Wow!

Simply put, if the interest rate on your mortgage goes up, your monthly payments go up. Pretty standard stuff here.

To avoid this potential problem, just go with a fixed rate mortgage instead of an ARM and you won’t have to worry about it.

You can also pay off your home loan before your interest rate is adjusted on another ARM. Or go with a fixed rate mortgage instead.

Or simply sell your home before the adjustable period begins. Lots of options really.

I had a 5/1 ARM in 2017 that I retrofitted to a 30 year fixed prior to its first maintenance. Looking back I am very glad I made the change.

Mortgage Payments Increase When the Interest Only Period Ends

- Your payment can also go up if you have an interest-only loan

- At that point it becomes fully amortizing, meaning that both principal and interest payments must be made

- It costs twice as much because you have been withdrawing interest for years before that

- This explains why these loans are not very popular today and are considered non-QM loans

Another common reason for increased mortgage payments is when the interest-only period ends. This was a common story during the housing crisis of the early 2000s.

Typically, an interest-only home loan is paid off in full after 10 years.

In other words, after ten years you will only be able to pay the interest.

You will need to make principal and interest payments to ensure that the loan balance is paid off.

And guess what – the full payment will be much higher than the interest-only payment, especially if you’ve deferred principal payments for a full 10 years.

Simply put, you pay off the entire original loan balance in 20 years instead of 30 since nothing is paid during the IO.

This assumes the loan term was 30 years, because paying only interest means the original loan amount remains untouched.

It can lead to a significant increase in monthly mortgage payments, forcing many borrowers to refinance their loans.

For example, a 3.5% IO loan with a loan amount of $300,000 would be $875 per month. After 10 years of making that payment, your monthly will jump to about $1,740. Almost twice!

Just hope that interest rates will agree when the time comes or you may be in for a rude awakening.

Tip: This is a common setup for HELOCs, which offer an interest-only period followed by a full payment period.

Mortgage Payments Increase When Taxes or Insurance Increase

- If your mortgage has an impound account your total mortgage payment can increase

- An impound account requires homeowner’s insurance and property taxes to be paid each month

- If those costs increase each year the total premium you pay may also increase

- You will receive an escrow analysis every year letting you know if/when this can happen

Then there is the matter of property taxes and homeowners insurance, assuming you have an impound account.

Recently, both have risen due to rising property prices and inflation. In California, many have even lost their insurance, leading to steep price increases for the state’s FAIR Plans.

Even if you have a fixed-rate mortgage, your mortgage payment can increase if property tax and insurance costs increase, and are added to your monthly mortgage payment.

And guess what, these costs tend to go up every year, just like everything else.

A mortgage payment is often expressed using an abbreviation PITImeaning principal, interest, taxes, and insurance.

With a fixed rate loan, the principal and interest rates will not change throughout the life of the loan. That’s good news.

However, there are situations where both homeowners insurance and property taxes may increase, although this only affects your mortgage payments if they are taken out of an impound account.

Keep an eye on the annual escrow analysis that shows how much money you have in your account, as well as the estimated cost of your taxes and insurance for the coming year.

It might say something like “the escrow account is short,” and therefore, your new payment will be X to cover that shortfall.

Tip: You can choose to start making a higher mortgage payment to cover the shortfall, or make a lump sum payment to increase your escrow account balance so your monthly payment stays the same.

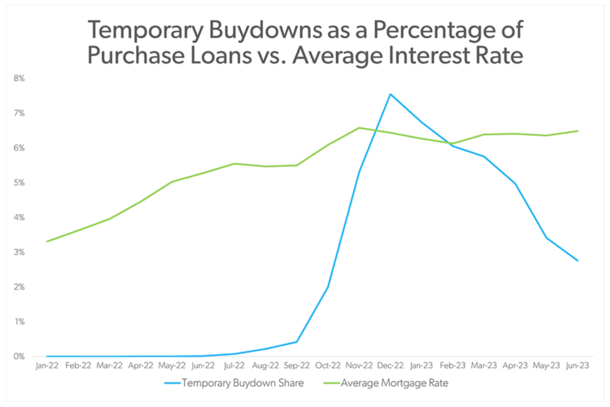

Your Mortgage Can Increase When the Purchase Period Ends

Here’s a bonus (and headline) reason why your mortgage will go up; temporary purchase. These have grown in popularity recently.

In fact, they peaked at a 7.6% share in December 2022, with Freddie Mac, which means many borrowers will face higher mortgage payments soon.

The way it works is you get a discounted loan amount for the first, two, or three years. Then your interest rate returns to the original value of the note, which will be higher.

The discount would be 3% discount in the first year, then 2% discount in the second year, and 1% discount in the third year. So if your rate was 6%, it will be 3%, 4%, 5%, and finally 6%.

For the remaining 27 years of your loan term, the undiscounted rate is 6%.

Of course, this is well documented and not a surprise, so you should know exactly what you are getting into, unlike ARM where the adjustment is based on market uncertainty.

However, if you don’t put in the necessary funds to get a high payout, it could result in some unwanted payout shock.

Prepare for a Higher Mortgage Payment

The takeaway here is to consider all housing costs before deciding whether to buy a home. And make sure you know how much you can afford before you start your property search.

You’d be surprised how costs can add up when you include insurance, taxes, and daily maintenance, as well as the unexpected.

Fortunately, the annual payment fluctuations associated with escrows will likely be small compared to the ARM’s interest rate reset or interest-only expiration.

It is often called because the difference is spread over 12 months and is not that big at first.

Although recently there have been reports of significant increases in property taxes and homeowner’s insurance premiums due to inflation.

So it’s still key to prepare and budget accordingly as your mortgage payments may increase over time.

At the same time, mortgage payments have the potential to decrease for many reasons, so it’s not all bad news.

And remember, thanks to our friend inflation, your monthly mortgage payment may seem like a drop in the bucket ten years from now, while tenants may not get that payment relief.

Read more: When do mortgage payments start?

Before creating this site, I worked as an account manager for a real estate broker in Los Angeles. My experiences in the early 2000s inspired me to start writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the mortgage process. Follow me on Twitter for the latest.

Source link

.png?w=390&resize=390,220&ssl=1 "Introduction: Why Commercial Lending Will Look Different Towards 2026")