If you hope to be released the speedy fannie mae and Freddie Mac, you might want to use some patience.

While the issues of the coservotristhip issues increased dramatically when the Trump’s second name begins, while the rising war.

One of the biggest points of adherence is the amount of a mortgage, many expect to increase if they are released.

Having a nearby subtle assurance that Fannie and Freddie will buy and protect the loan that will make you cheaper.

Expectation If / Associates to the community, the mortgage tax prices may require more to compensate the growing risk.

Fannie and Freddie were in a Conservatorship problem since 2008

First is the quickest background. After the worst housing problem in the latest history, Fannie Mae and Freddie Mac, known as government-sponsored businesses (GSES) placed in Conservatorship.

This was actually a government balout as these were the only ones being “severely damaged ‘because of the restoration of the first embryo of 2000s and” they cannot carry on their journey without government. “

The planning allows them to continue supporting the most fragile housing market as it is recovering 10 years ago.

But maybe no one expected that these were alone and stayed in the hands of the government as long as they had it.

In the last planning, now it’s been 20 years! Of course, this is not the first efforts that have been done to release them in the wild.

During the first Trump name that started back in 2017, there were a lot of issuing talk. And both company shares respond appropriately.

They would trade in the type of £ 1 at the end of 2016 and rapidly riser to more than $ 4 for each assignment in early 2017 before the end.

As soon as Fannie Mae and Freddie Mac country lost steam, they eventually became shary shares.

A lot of investors to investors around their release

Like the past eight years, there have been a lot of consideration for investors around their release, which is contradictory is part of the problem.

It seems that people are more interesting in making Buck to trade than to think the true meaning of their outflows. GO FICETSO …

The latest Visible Gold Rush is investor Bill Ackan, manager of Square Capital Management “can be familiar for 180 million shares in two companies.”

It is reported that you see a $ 1 billion benefit in the investment, and the shares that rise around $ 34 post-post-post-post-post.

For a clue, they are currently selling $ 6 per $ 6, so it can represent real gain.

It is like the conditions before Trump’s first victory over the President, these couples traded in a $ 1 grade.

But they were very up, and two FNMA and FMCC risen about 500% since Trump has achieved the second term and speculation about their exempt.

As noted, this conflict of interest is currently played. And the same issue we saw in the past eight years. It is the stock market instead of “Hell, is this good in our country?”

Fannie and Freddie’s release will enhance impact on maximum tax prices

While investors hope that the couple are released and make informed wealth, We should only let them go if it is safe and appropriate to do so.

If SecoCott Bessent is recently established, who also is the new director of the Consunder Protection Burderu (CFPB) doing good, that may not be time.

In a conversation with Bloomberg this week, when asked about their release, it means, “currently finding it, then we will think about that.”

He also added that “the most important in Frannie and Freddie is issued, the most important metric I want or the idea that the maximum tax rates will increase.”

“So whatever it is done around secure and aloud relation will decrease the effect of long-term loan price.

Simply put, he and those around him know that the mortgage prices can rise when Fannie and Freddie were forced to stand alone.

And because the tax rates come from about 3% to start about 2022 to 7% today, the last TRUM management seekers.

Therefore, it actually stabs down to help investors to be rich or help daily Americans buy home-based homes.

It will be a happy decision …

The couple should be released, but probably a little after reducing their foot cords

My thoughts on this issue is that the couple are not ready for the release. There is no lot that has changed since continuously under help, without the quality of cooperatives.

Indeed, they do not have nearly difficulties that are about the default financial and predictions, but continue to return most home loan in the United States.

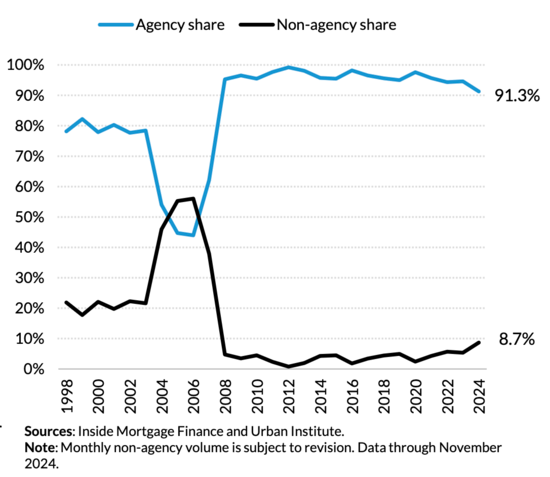

See the above chart from Urban Institute. More than 91% of MBA’s release is an agency – supported by an agency, including Fha and VA. But about 40% of the first Lien’s Gse, while 4.1% secret-label.

Without them, there will be turmoil in distributed markets. Or extracted, there may be a chaotic.

However, they should be released at a particular time if they are real public companies, not government agencies.

The best way about walking may have significantly lowering its feet before it happened (apologizing for investors).

To do so, they can return or stop buying and protecting the achievement of two homes and investment buildings.

In other words, limit their residence options in daily homeworks without those who buy a second, fourth, fourth or five.

It is amazing that this may be comfortable with sale sales, which has attacked the housing market at least 10 years ago.

There may be additional changes in the menu of their product menu, which will be small, for the purpose of marketing confidential investor.

As Fannie and Freddie find small, private players can grow hundreds and play over the passage.

This will reduce our trust in that couple, and reduce the impact of their final issues.

(Photo: Virginia State Parks)

Before creating this site, I worked as an account official because of the seller of the sales asset in Los Angeles. My first experience of 2000s encouraged me to start writing about 19 years ago to help the consumers that would be better and better. Follow me on Twitter to take it.

Source link

.png?w=390&resize=390,220&ssl=1 "Introduction: Why Commercial Lending Will Look Different Towards 2026")