Credit stress data

When the next recession of job losses happens, we will see an increase in the credit stress data and I am 100% sure that the American destroyers will stay in their useless things. YouTube again X accounts, relentlessly pushing their negative narrative. However, now that you have all the information, you can see that the credit stress data we saw in the 2008 crisis will not happen again as long as we have the right mortgage. My crusade over the last decade has been about making sure that lending standards don’t loosen because standards are looser today, but not crazy anymore.

The reason I fight so hard on this premise is that if we have an economic stress like we saw at the start of COVID-19 and the big burst of inflation, home owners will be protected by their boring vanilla 30 year mortgages.

With the data line below, I expected that we would return to pre-COVID-19 levels of credit stress by the end of 2024, but that did not happen. Also, everyone pushing 2008 housing needs to get out of it.

Please use these updated charts on credit data in your Thanksgiving dinner conversation and remember why this is so important. New listing data we track Study of Altos trending at the lowest levels during the last few years, while at that time it was operating at accelerated levels. Here’s an example with our data from Nov 9. Look at the difference between this week of 2024 compared to the same weeks in 2009-2011. We had many distressed sellers at that time!

New listing data this week:

- 2024: 48,863

- 2009: 274,614

- 2010: 359,534

- 2011: 315,915

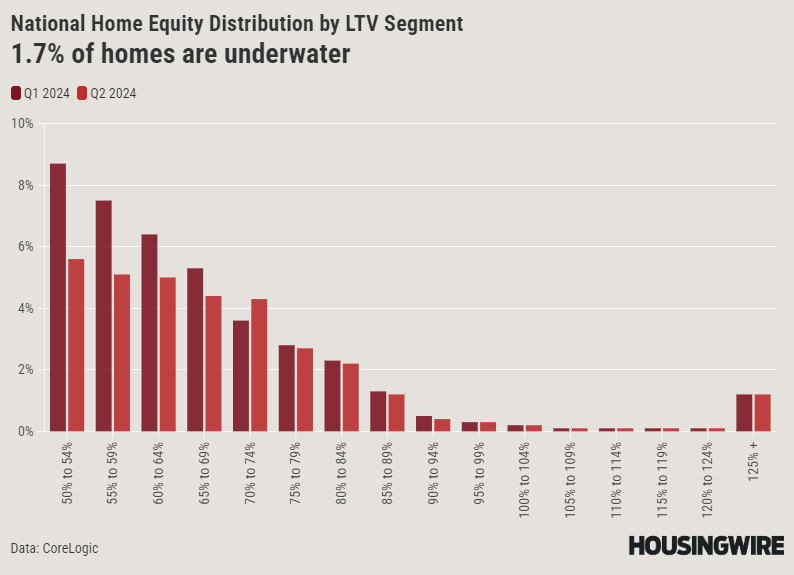

These credit-stressed sellers did not turn around and buy another home, thus creating years of high stress availability in the market. This hasn’t happened once in the last decade, and it won’t happen until we see a recession of job losses. Also, back in 2010, more than 23% of homes were underwater; today, it is the lowest percentage.

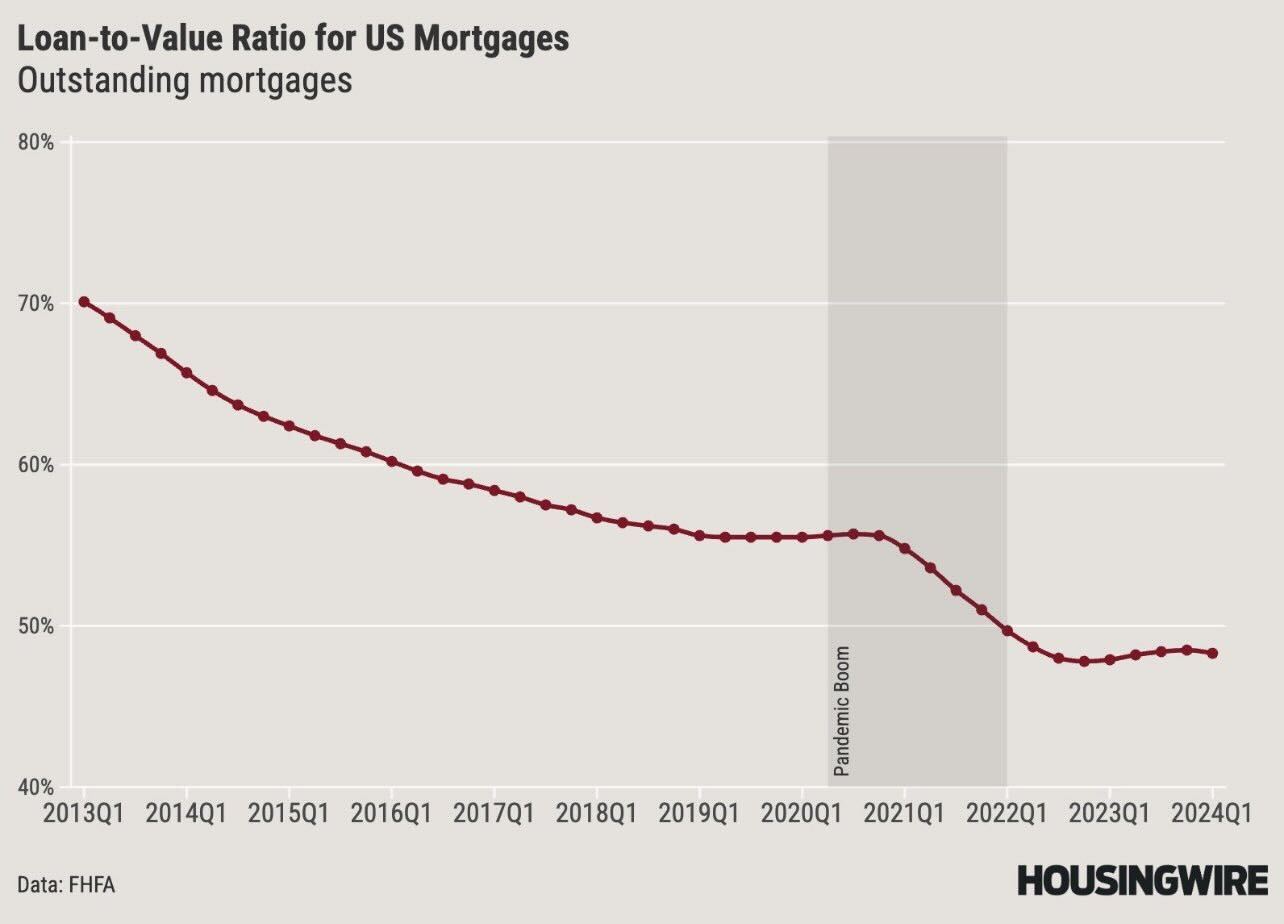

Another thing to consider: more than 40% of households currently do not even have a mortgage and loan-to-value ratios for those that do are less than 50% on average. In 2008, the loan coverage was around 85%. Plus, this year’s median down payment is 15%, which means homeowners have more skin in the game than ever before.

Hopefully, all of these charts will clear up the confusion for your Uncle Dave and any other Thanksgiving guests who think we’re going to see another housing crash like 2008. Homeowner credit data tells a different story.

Source link

")