Do we really want to retire with a powerful retirement strategies to generate more than indigenous programs? – Resources Center for Retirement

Eliminating a small distribution required makes Roth 401 (k) very important.

Something found me. Protected law of 2.0 has finished the minimum distribution required (RMDs) of ROTD 401 (K) s. When you first look, that change seems harmless. After all, accounts owners pay taxes before, so why did you force them to withdraw their money. That’s fake mistake that the goods in the Roth continues to produce tax returns, whether the account holder has reached 73 – years when RMDs drag the traditional plans. That ability to continue to save free taxes make the most important roths.

The immediate refreshment of the other called equity between traditional and religious systems can be a good way to clarify what has happened. Under the Traditional 401 program in contrast, initial donations in rathers are not charged, but the interested interest receipt is free and no taxes paid when the money is damaged.

Although traditional plans and pornifers can sound very different, a common argument that they provide the same tax benefits. Unfortunately, the easiest way to show that this point has equations. Take that t is the amount of the individual’s side tax and guard Is the year’s return of the property in the system. If one gives $ 1,000 in the traditional system, then after ni Years, Balance has not grown into $ 1,000 (1+guardSelectedni. When a person can withdraw a collected, the first contribution and earnings of taxes are taxed. Therefore, the amount of tax after retirement (1-t) $ 1,000 (1+guardSelectedni.

Now think about the Rota. Each person pay tax in the first stage, so you put (1-t) $ 1000 to the account. After years, this ends afterwards would be up to (1+guardSelectedni (1-t) $ 1,000. As income is less than any additional tax, post-tax prices under the traditional Roths are the same as:

Note that the main thought of this work is N – the number of years of accumulation – is similar in both cases. That was true. In both cases, the limited tax contains tax. Now “n” is not the same as a traditional and roth 401 (k) s. Traditional programs should begin to remove their money in 73; Roths owners have never taken their money. (The rear distribution distribution rules are still valid.)

One conflict of changing RMD rules seem to have been making a roth 401 (k) treatment with Roth Rath treatment, which is not less than RMMS treatment. Consistency is a good goal. Congress is simply shown in the wrong way.

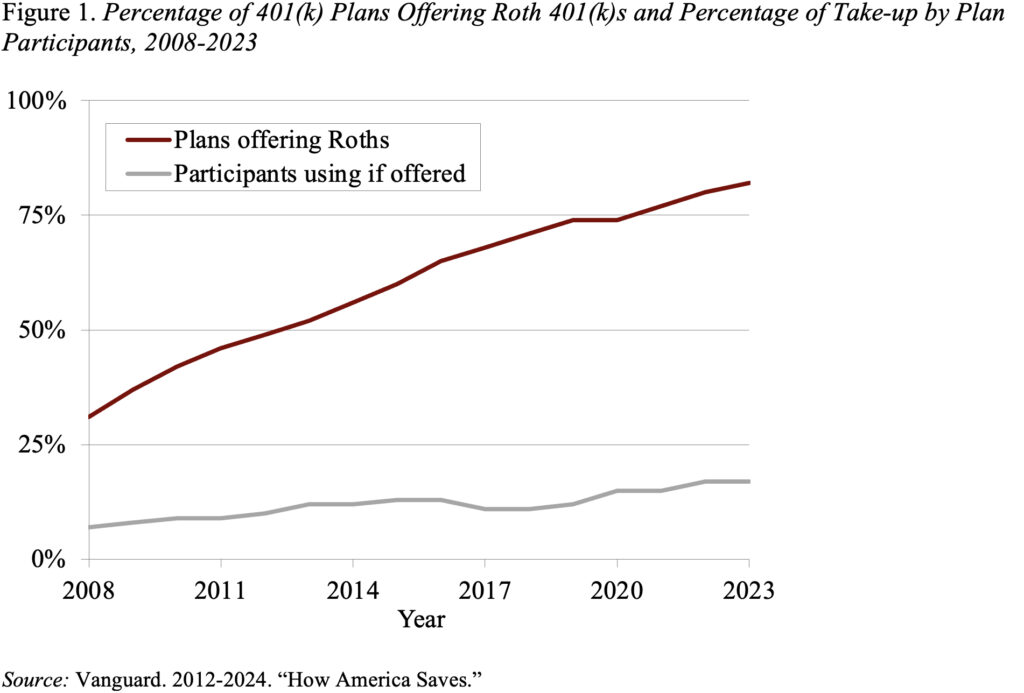

The wrong way is cost government money. Currently, whether 82 percent of employers donate to Roth 401 (k), only 17 percent of participants take donation (see Figure 1). As many employees see the benefits of No RMD, the percentage will increase. As a result, retirement tax evasion – expenditure tax revenue – expenditure under any state – will increase. If Congress wants money, it launches RMDs Roth Iras and returns ROTDs of Roth 401 (K) S tax benefits only but also raise funds. That should be a good thing!

Source link