To say it’s been a bad 12 months for housing sales would be a gross understatement.

Today, the National Association of Realtors (NAR) reported that existing home sales fell to their lowest level in nearly 30 years last month.

So if you’re wondering if something is broken after the Fed raised rates 11 times, look no further than the housing market.

According to the NAR, existing home sales fell to an annual rate of 4.06 million in December, the lowest rate since 1995.

To get an idea, most real estate agents today were not born in 1995, and they are loan originators who help consumers get loans.

What’s Causing a Decline in Home Sales?

While home sales are very close to closing in 2024, annual volume was the best and worst since the mid-1990s.

Driving the lack of home sales have been two main factors. Lack of merchandise and lack of affordability.

And one could argue that mortgage rates are behind most of it, even if it’s the mortgage rate lock that’s causing homeowners to stay put.

Even lower mortgage rates were seen in 2021, leading investors and others to hoard what little there was and refuse to let it go.

Now that 30-year mortgage rates are around 7%, it’s becoming unaffordable for new buyers to enter the fray.

NAR noted that completed transactions, which include single-family homes, town homes, condominiums and co-ops, increased 2.2% from November and 9.3% from December 2023.

That was the third month of year-over-year gains, but still not enough to raise the annual total by any significant amount.

Granted, the annual rate is over four million, a little bit, so it could have been worse I think. But it sure wasn’t good.

The NAR reported that total housing starts at the end of December stood at just 1.15 million, down 13.5% from November but up 16.2% from one year ago (990k).

That means the net unsold at the current sales pace was just 3.3 months’ supply, down from 3.8 months in November and up slightly from 3.1 months in December 2023.

Home Prices Continue to Rise Despite Sales Risk

As we all know, home prices are driven by supply and demand. If there is less available, the price goes up, assuming there is more demand than supply.

While demand has also been muted due to a lack of affordability, it has not weakened enough to offset further gains in home prices in many markets, hence the commendable numbers for the rest of the country.

Roughly speaking, the median price of an existing home rose to $407,500 in 2024, up 6.0% from last year’s $381,400.

And it could just be driven by the Northeast or another tropical part of the country. All four US states posted YOY price increases.

The Northeast was the strongest with home prices up 11.8% from last year, followed by the Midwest (+9.0%), the West (+6.0%), and the South (+3.4%).

Many people believe that there is an inverse relationship between home prices and mortgage rates, but it’s really an inverse relationship.

The lower the loan rates, the higher the transaction. But when prices go up, you see home sales slow.

That doesn’t mean home prices are falling though. They can and will continue to rise as long as supply does not stack up.

Generally, anywhere from 4-5 months of supply is considered a healthy, balanced housing market.

We continue to see supply in the 3 month range, which is not enough, although it does prevent home prices from falling.

Why It’s Good to See Home Sales Decline

While low home sales are obviously bad news for many reasons, namely that the economy is often driven by real estate, there is one good thing.

We know that housing today is rarely as bad as it was in the 1980s (remember double-digit home prices?).

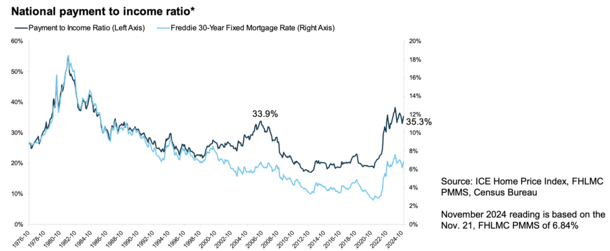

Home buying conditions are currently worse than what we saw at the height of the housing boom in 2006.

During that time, the national average pay and benefit increased to 33.9%, per ICE. Since November, it has increased by 35.3%.

Much of it was driven by very high mortgage rates, which rose from around 3% to as high as 8% in 2023 before falling to 7% now.

As noted, house prices have continued to rise despite this, albeit at a slower pace.

The combination of a high asking price coupled with a loan amount that is more than double what it was has been a one-two punch.

However, the market responded appropriately. Back in 2006, home sales continued to boom and bust.

Why? Because we had absolutely no oversight in the mortgage world. Instead, we have adapted by offering riskier and riskier loan products, as well as stated income and no-doc underwriting.

Today, much of that is gone because of the changes made after the crisis of the early 2000s.

You can thank the ATR/QM rule for removing many of those factors, which have made today’s housing market sound.

Sure, housing sales will continue to suffer, but at least we don’t have new loans and mortgages going to people who can’t afford them.

Read on: The risk factors of the housing market are very different today.

Before creating this site, I worked as an account manager for a real estate broker in Los Angeles. My experiences in the early 2000s inspired me to start writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the mortgage process. Follow me on Twitter for the latest.

Source link

.png?w=390&resize=390,220&ssl=1 "Introduction: Why Commercial Lending Will Look Different Towards 2026")