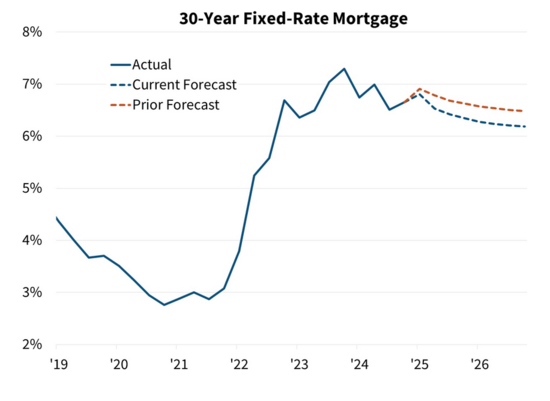

Fannie Mae now expects mortgage prices to become 30 points at the end of the year

The latest weather conditions from Fannie Mae is a good thing, thinking you are a home buyer or the existing landowner.

Government funded ENTERPRISE (GSE) reduced its predictions properly since last month.

They now expect that Year of 30 years is scheduled to be 30 low-total point at the end of 2025. And 30 points are at the end of 2026.

Instead of 6.6% of the closing of 2025, they are now seeing the age of 30 falls to 6.3% instead.

This should come like acceptable news to anyone who wants to maintain a mortgage in the mortgage.

Less than 10 years fruit = low-lying level forecast

Fannie Mae saw that the Harbor crop for 10 years “pulled back” at the levels just seen about mid-January.

Therefore, now they expect that the number of prices are low from less than 10 years yields we translate advertised tax prices.

That happens in accordance with Trump’s opening. It seemed to be sold for a news event, where he had accessed office shares and the bonds began to meet.

Of course, this is conducted by the immense economic view, so it can be bittersweet news.

In other words, you may be able to pull the lowest interest rate but your job security can be very bad. Not quite the best trade in the world.

Fannie Mae appears to use primary 10-year bond crop to come up with their monthly loan status.

And because he has fallen nearly 25 points, reviewing their recognition by the same value.

Instead of 6.6% by the end of 2025, they now expect an average of 6.3%.

Their 2026 weather forecasts and improved 30 points (.30%) from 6.5% to 6.2%.

Fannie has never been very aggressive in their prediction, as they are simply having a crossing rate from 6.3% in 2025 to 626 in 2026 in 2026.

But I look for a trajectory over real statistics to get the idea of what prices can go.

In other words, they may actually go very low than Fannie expecting them to give their status. And when the 10th year yield continues to fall, Fannie will continue to renew their predictions.

Note that they review these numbers every month, so their forecast is always changing, not one-off a year such as my annual wish anniversary.

Interestingly despite Fannie projects some projects are determined by September, followed by extra cuts in 2026.

At that time, the CME flewatch still has three level cuts for three years in this year only. It is not that the Fed Control rates are great, but Fannie can play it safe here.

Standard ton of uncertainty held around the surroundings

To accomplish that, they say, “there is uncommon uncertainty about how to grow and inflation during the remainder of our seed ratings.”

I have expressed this idea recently because it is so much in the air, whether it is the life government, the ongoing trading war, and international taxes.

This makes it especially difficult to predict the number of prices for partners, especially when they are already difficult to predict starting in the normal place.

When it takes down, most of the annual loan predictions find the time and time.

They were wrong when the mortgage prices called records (they expected to go up) and were wrong when they hit 8% (unauntalled to travel.

So it will never be a good idea to put a lot of stock in the predictions.

However, the growing feeling of low prices later this year seems to take speed, and can indicate that they will actually be low.

In My 2025 Revenue Rate Forecast Rate Forecast Post, I said that 30 years of repair would be less than 6% of the fourth quarter. Specifically, I said 5.875%.

I still believe that will happen, even though UncertaintyWhat appears to be the keyword recently, can cause the amounts to jump around high levels for a while.

And they can prevent them from long, or eventually decrease when it is solved in the dust.

Finally, financial lenders and MBS investors do not want to be surprised, so prices will continue to monitor the visible future.

Remember, the lenders are quick to raise prices, but they always take their delicious time to reduce.

However, because of this district loan scenery, the Fannie expects a domain loan volume for 10% to $ 1.4 trillion (up $ 12 billion from previous month).

They also expect the volume of a cleaning loan to increase $ 502 billion in 2025, raising $ 38 billion from their prediction in February.

Good news for both loans and home consumers and homes.

Learn to: Do I have to wait for a mortgage rates to throw away before buying a home?

Before creating this site, I worked as an account official because of the seller of the sales asset in Los Angeles. My first experience of 2000s encouraged me to start writing about 19 years ago to help the consumers that would be better and better. Follow me on X by taking hot.

Source link

.png?w=390&resize=390,220&ssl=1 "Introduction: Why Commercial Lending Will Look Different Towards 2026")