In the world of mortgage rates, sometimes it’s a game of inches.

This can be true for both prospective home buyers and existing home owners looking for price relief.

Granted, if you’re on those limits when it comes to buying a home, maybe you should consider renting until you’re more settled.

But if you already own a home and have a high mortgage rate, the next six months can make or break your chance to repurchase.

Recently, mortgage rates have bounced back from their recent decline of just over 6%, returning to levels around 6.625%.

As a result, many millions of homeowners are no longer “in the money” to renovate. But that can change in an instant, as it has.

Are Current Mortgage Rates 0.75% Below Your Rate?

A new report from ICE revealed that the number of people working again increased to more than 4.3 million due to the rate meeting that came to an abrupt end, ironically after the Fed’s rate cuts.

At the time, the 30-year mortgage was averaging 6.125%, down from around 7% as recently as late July.

That meant that the number of people able to be updated increased from 1.2 million to 4.3 million in less than two months.

Of these 4.3M, 65 percent received a loan in the past two years, including 1.4M in 2023 and 1.3M this year. So that every day is the level, marrying something of the house may actually pan out.

ICE considers a homeowner “in the money” for value and refinancing if their mortgage rate is at least 0.75% below prevailing market rates.

So any borrower with a 7%+ rate would have met that definition by mid-September.

But today only those borrowers with mortgage rates around 7.5% can benefit from the refi.

If you want to get more into the nitty-gritty, the most qualified finance candidates should have a 720+ FICO score and a loan-to-value (LTV) ratio of 80% or less.

Of course, conditions can change quickly. And as I wrote the other day, mortgage rates don’t go up or down in a straight line.

Which means the recent uptick could be a temporary hiccup and it’s short-lived. Mortgage rates have seen periods of relief on the way up. They saw moments of pain on the way down.

Refi Boom Leans on Levels to Continue Low in 2025

As you can see, even small rate changes can affect millions of homeowners looking for down payment assistance.

The good news is that ICE expects 30-year mortgage rates to continue to decline in the final months of the year and into 2025. For the record, I agree with them.

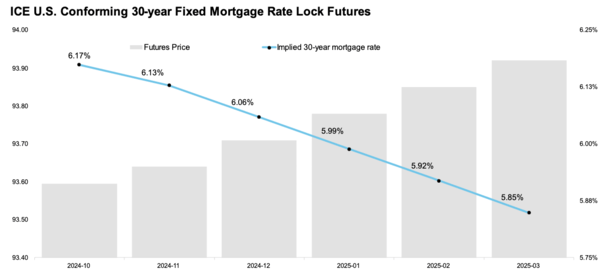

Their latest rate, calculated using the one-day spread between the loan balance’s weighted average future APR rate and the simple one-day rate, has the 30-year down to 5.85% in March 2025.

Admittedly, it also has a 30-year fixed at 6.17% through October 2024, so some recent corrections may not have been captured by their time-sensitive report.

But as noted, it’s good to step back anyway, and pay a little attention to the day-to-day or week-to-week noise.

A lot can happen in a few days, and we have two big reports coming tomorrow and Friday, the CPI report and the PPI report.

Both are likely to push prices back to their bottom line. They may also raise prices higher…

If the ICE forecasts hold for a long time, there will be a good refi boom for loan officers and real estate sellers in early 2025.

Rates may also approach the so-called magic number of 5.5%, at which point you’ll find more homebuyers entering the market again, perhaps in the springtime.

This is a bullish case for the mortgage market, but it is still very high in the air. You can see how everything changes even a .125% or .25% difference in the rate can affect millions.

Read on: Refinance rule of thumb.

Before creating this site, I worked as an account manager for a real estate broker in Los Angeles. My experiences in the early 2000s inspired me to start writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the mortgage process. Follow me on Twitter for the latest.

Source link

.png?w=390&resize=390,220&ssl=1 "Introduction: Why Commercial Lending Will Look Different Towards 2026")