Although low mortgage rates have also bolstered optimism for a sluggish housing market, 2025 may not be much better than 2024.

Sure, low interest rates improve affordability, but there are other parts of buying a home that remain affordable.

Whether it’s an unaffordable asking price, or rising insurance premiums and high property taxes. Or other monthly bills that eat into the housing budget.

This explains why the forecasts of mortgage origination for purchase loans continue to be very negative.

However, the emerging trend of increased mortgage refinance volume should be strong in 2025.

2024 Buying Volume Revised Down

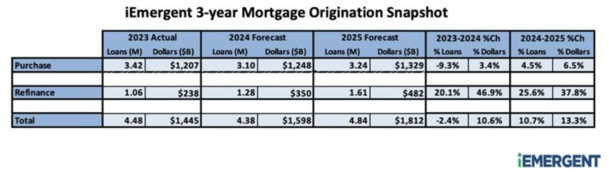

A new report from iEmergent revealed that mortgage purchases for 2024 are expected to decrease in terms of loan volume compared to 2023.

In other words, despite lower mortgage rates, the number of home loans now expected to fall below 2023 levels.

However, due to the increase in average loan size, the company believes that the value of purchase loans will still increase slightly by 3.5% year over year.

Still to be blamed is the mortgage rate, which rose almost a year ago and is now down about 2 percent.

But home prices remain high, and when combined with 6% mortgage rates and rising insurance premiums and rising property taxes, the math is often out of whack.

Adding to the affordability problem is the continued lack of existing housing supply. There simply aren’t enough homes for sale, which has kept prices high despite declining demand.

Refis Expected to Jump Nearly 50% from 2023 Lows

On the other side of the coin, mortgage repayments are finally showing strength as a result of lower mortgage rates.

They expire in late 2024 when the 30-year rate hits the 8% mark, with only a handful of cash outs making sense for those who need help paying off (other debt).

But since then the rate and time repayments have increased significantly as the latest mortgage benefits fall into the “money” savings of monthly payments.

As noted last week, rate and term refinancing rose 300% in August from a year ago and refinancing as a share of total loan production rose to 26%, the highest figure since early 2022.

It is likely that it will continue to grow until 2025 as mortgage rates are expected to drop significantly this year and next.

iEmergent said they “expect prices to finally begin to decline in the coming months,” on top of the roughly 2% decline we’ve already seen.

While many have argued that the rate cut is largely focused on mortgage rates already, which explains the rise in mortgage rates after the Fed’s tapering, there is still a lot of economic uncertainty ahead.

A 50 basis point came as a surprise to many and another could be on deck in November, currently holding a 60% chance per CME FedWatch.

If it turns out that the Fed got behind the eight ball, the yield on the 10-year bond (which tracks mortgage rates) could drop further than it’s already penciled in.

At the same time, there is still room for mortgage spreads to tighten as the market adjusts and adjusts to the new low rates (and previously high loan volumes).

2025 Funding Volume Set to Increase Another 38%

Looking ahead to 2025, the refinance picture is expected to be even brighter, with those loans increasing by 38% (in dollar terms) from 2024.

This will likely continue to be driven by rates and term restructuring as interest rates continue to improve and millions who have taken out loans from 2022 take advantage of cheaper rates.

But it may also come in the form of refinancing, which will be even more attractive.

Even if an existing homeowner has a rate of 4%, something in the high-5s or low 6% range can work if they need cash.

This could be an indication of increased debt in other departments, as savings during the pandemic dry up.

Ultimately, homeowners haven’t touched their equity in this housing cycle, so there’s an expectation that will happen at some point, especially with home equity in the highest neighborhoods.

You may also see this in the form of second mortgage, HELOC rates that are expected to drop another 2% as the principal amount is reduced by that amount over the next 12 months.

Meanwhile, iEmergent predicts a modest 6.5% increase in consumer volume by 2025, pushing dollar volume growth to just 13.3%.

As to why mortgage lending is expected to decrease significantly next year, it is a broader economic issue.

If economic growth continues to slow and a recession occurs, a weak labor market with high unemployment could dampen demand for home buyers.

So even though mortgage rates are dropping significantly as a result, you have fewer willing and able buyers, despite the lower monthly payments.

This explains the phenomenon of how house prices and mortgage rates can go down in tandem.

They may not, but at least it dispels the idea that there is an inverse relationship between the two.

Long story short, 2025 should be better for mortgage originators because of refis, but don’t get your hopes up for mortgages by seeing a big jump due to low rates.

Before creating this site, I worked as an account manager for a real estate broker in Los Angeles. My experiences in the early 2000s inspired me to start writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the mortgage process. Follow me on Twitter for the latest.

Source link