It seems clear that the housing market is decreased, and now it is a consumer market than the seller’s market.

While this makes it and will always vary.

All of this is related to recording available available, which has made it difficult for a home buyer who will attend the COUNT Pencil.

Maximum stubborn loan amounts do not help the story, call the question if it is a good time to buy a home. Or if it is better to continue hiring.

But if you pass by home shopping today, you expect to keep the property for many years to come.

Home prices are cool and may go wrong this year

While CoreLogic economists still predict the prices of household prices to increase the price of January 325 to January 2026, it seems that the benefits are slow.

And in some markets, especially Florida and Texas, the prices of local prices are already in the wrong and starting one year.

For example, local prices were issued by 3.9% YOY in Fort Myers, FL, 1% on Fort, TX, and 1.1% in San Francisco.

I expect that many markets turn into it as good as they make progress in 2025, especially with many future structures in the market and sitting on the market as the dom.

It is a simple issue of supply and demand, few (or interested) buyers, and many options.

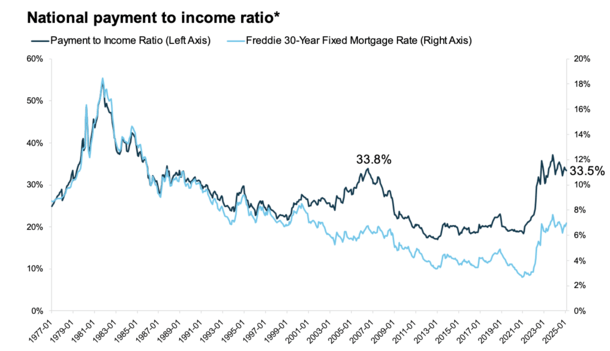

There are many oxen, but especially is a financial problem, with national payment in Income Ratio is still around GFC Bubble High, with each snow.

This means why home shopping systems are still good in spite of the recent loans.

Sprinkle on the Insurance Insurance and property taxation, as well as the daily cost of living and it becomes very difficult to buy home today.

While it is possible to be the best buyer’s good news.

If this progresses, I expect the construction of the prices at home, although the mortgage prices can fall from Tandem again.

Nevertheless, I did not expect good gain after the home purchases today in many cases.

Appreciation is expected to be a beautiful apartment in many marketitors for the visible future.

This means that the only way to make a dent has normal difficult payments (one of four important items in sector).

Your loan is a little bit paid when higher amounts

| $ 400,000 loan loan | 2.75% of the loan level | 6.75% of the loan level |

| Monthly payment | $ 1,632.96 | $ 2,594.39 |

| Interest paid in 3 years | $ 31.938.47 | $ 79,698.01 |

| Principal in three years | $ 26,848.09 | $ 13,700.03 |

| Remaining left | $ 373,151.91 | $ 386,299.97 |

The problem is the loan amount now today is close to 6.75%. In cash loan amount, which means only $ 345 for the first payment to the principal.

$ 2,250 left to interest. Yes, you read that privilege!

As a result, your loan is paid a little bit today when you release home loan.

Compare this to the people who take out small amounts of 2-3, with small amounts of loan and the highest payment.

In the same amount of loans $ 400,000 in 2.75%, $ 716 toward the principal and $ 917 reaches interest.

The result is that homeowners get equality, and they create a comprehensive buffer between what they owe and how appropriate their home.

Returning back to 6,75% of our loan, they can still owe $ 386,000 after three ownership years.

The lowest payment makes it difficult to sell your home

Now let’s pretend that the 6.75% of the loan holder puts 3% off their home footback.

This is a minimum of Fannie Mae and Freddie Ma, the most common type of mortgage (agreed on the loan).

The price of purchase will be about $ 412,000 in this situation, which means $ 12,000 paying down.

It is good that the lower pay is low I think, but it also means you have very little equity.

And as shown, you will pay less than 36 months of home.

Three years, the balance will decrease over $ 386,000, which is Cushion of about $ 26,000.

At normal occasions, we can expect the prices of local prices to increase about 4,5% per year, set up a Court of Court for $ 470,000.

This will give our Home Houses Home to about $ 84,000 in domestic equivalent, among the appreciation and your payment.

That works about $ 58,000 in informa, $ 14,000 in Princilt, and $ 12,000 down.

Now let’s think you want to sell because you don’t like the house for any reason, or you need one different, or simply you cannot afford it.

There are many charges of transaction involved with selling a home

| $ 412,000 Home Purchase | 1% benefit annually | 4.5% Benefits every year |

| The amount after three years | $ 424,500 | $ 470,000 |

| Balance after 3 years | $ 386,000 | $ 386,000 |

| Local Sale costs | $ 42,500 | $ 47,000 |

| Sales continues | – $ 4,000 | $ 37,000 |

Selling a home has no work. It comes with a number of transactions, whether it is able to transfer taxes, fees, title insurance, Real agent commissions, moving costs, etc.

While these fees varies with a Locale, one can expect divorce with 10% of the sales price at the cost of absolute closing.

So let’s pretend the home is able to sell for $ 470,000 after three years. Selling costs are $ 47,000.

This means that the active sales price is $ 423,000 low. You travel for $ 37,000 in your pocket, the difference between that and the rest of the $ 386,000 loan amount.

Remember that you are dividing with $ 12,000 to buy a place, so your “Profit” is $ 25,000. Or less when looking after you have paid your loan.

Now think of the home is not thankful for the amount 4.5% per year, and instead we thank 1% a year.

Costs $ 424,500 after three years and wants to sell it. The same 10% of the cost sales apply, reduces the amount at $ 382,050.

But you owes $ 386,000 to a mortgage. Although you do not have less water loan, where the balance exceeds home value, where the sale of sales are important, they are bad.

You will have to bring money to the table to sell the property.

For this reason, you need to think about a long time when buying equipment today.

This does not mean that the prices of the domestic will not increase in the next three years, but you can easily see how this can come.

In recent years, home prices increased twice a year, with 50% of the total revenues three or four in other cases.

At the same time, these householders were paying on their impairment measures as soon as possible due to the Londion of 2-3%.

This has made it a lot, very easy and quick to turn it fast and selling it. Or had to.

Now you may be stored for many years if you want to sell the benefit. So make a decision wisely.

Before creating this site, I worked as an account official because of the seller of the sales asset in Los Angeles. My first experience of 2000s encouraged me to start writing about 19 years ago to help the consumers that would be better and better. Follow me on X by taking hot.

Source link

.png?w=390&resize=390,220&ssl=1 "Introduction: Why Commercial Lending Will Look Different Towards 2026")