Today we will briefly consider the history of lying quality to find the small context where we stand today. It always helps to know that before you can be better guess what may come back.

About everyone who knows that the mortgage rates that hit all time records in 2021. But do you know which prices are being held in the early 1900s?

20-year 30% of 2.65% banned on Sunday ends on January 7th, 2021, low point in history.

Later that year, 15 years were under the lowest point, sinking in 2.10% during the week ending on July 299, 2021.

Some lucky owners are able to mount off-range rates under 2% for 15 to 30 years!

Freddie Mac loan loan statistics started in 1971

- Most of the funding statistics in prisoners are tied to Freddie Mac’s Archive

- Unfortunately, it goes back to the 1971 Year

- I wanted to dig down deeper to see what things like before 70s

- And see if I can receive data from the beginning of the 20th century to get additional perspective

The above figure comes from Freddie Mac’s Revenue Survey Survey, from 1971.

According to the record, back in April 1971, first month they began to track 30-year prices, the national average was 7.31%.

It went up as 18.45% In October 1981 and is low as 2.65% January 2021. It’s a real grade, apparently.

As you can see in the chart, those 18% loan amounts are short, as it was small loan prices. Eventually, they can be viewed as strikes in good plans of things.

Fifteen Reproduction Followed by Freddie Mac from September 1991, where values are found 8.69%. That same month when the 30 years are reached 9.01%.

Nevertheless, I remember a while back when the rates are set up to 4% of the grades going to travel with how many times since the 1950’s.

Why I made me wonder; Where did they even pull those historical information?

I never took time to see how the lower prices returned at that time, but I finally decided to do something to dig for more information.

Long history of the loan amount

- History of borrowed goods stretched back almost 100 years

- But the best records returned back to the beginning of the 1970s

- The 30-year repairs received in favor of the 1950s

- And prices reach the lowest in about 1945 before beating new sounds in 2021

My quest to find deep luxury history

Unfortunately, the details are still quite united. You see, back where there were different types of money laundering, not exactly what we use today.

When I don’t know that the first 30-year-old money is created), that is believed to be in the 1950s.

Before that time, it was a common tool for organizations such as trading banks and life-in companies to remove the temporary balloon-term loan.

These holes are often prominent to the principles of short loan loan as a three to five years, will also be reduced and unprecedented.

These loans are also written down in LTV measures around 50%, which means it was difficult to get home loan without low pay. In other words, homeowners are reserved for the wealthy!

Later, when severe oppression was beaten, home prices are recognized and the predicted funds filled the housing market because no one could make capital payments, especially if they had no jobs.

Then the new FDR covenant, which included a home loan association (HOLC) and the National Department of Housing 1934, both aimed at housing.

Holc, which was founded in 1933, would explain why the long Fixed-Rate loan is present today.

The purpose of the Holc was to enhance the old loan fees to long-term, fully paid, conditional, informal, 25 years. It is not far from the restoration of 30 years we enjoy today.

In a sense, it reminds me of the most expensive program of homes (HARP), which is lowly millions of millions of commeroal loan during the Great Financial Disaster (GFC).

It seems that some things do not change, even though we think they are different from this …

Money tax rates to decline as loans and ltv rises

- Home Convership was very reported later due to three main objects:

- Low interest rates

- Terms of a long loan

- And high ltvs (low payments)

In 1934, FHA and Federal Galings and Lovan Insurance Corporation (FSCIC) was created, and in 1938, Fannie Mae was born.

All of these frameworks increases the credit funding basically and led to the free loans of home consumers.

In time, the mortgage values drop while LTV ratios and loan amount has risen, as you can see the charts below.

This has made that Home Comership readily available for everyone, not just those who have the power to bring a great pay for the table.

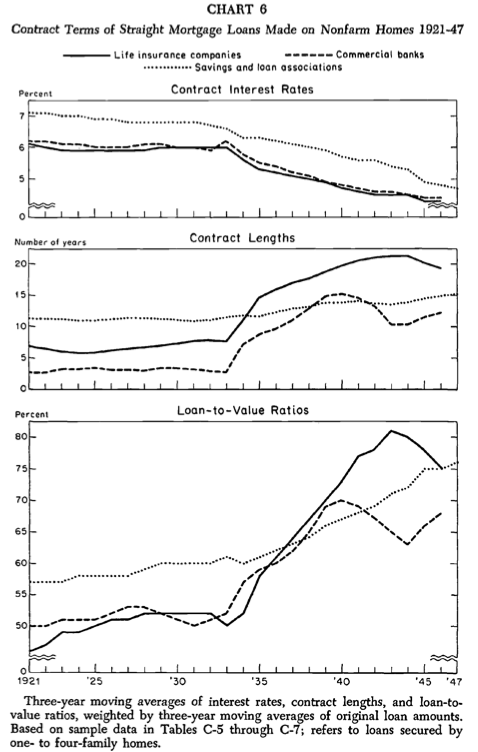

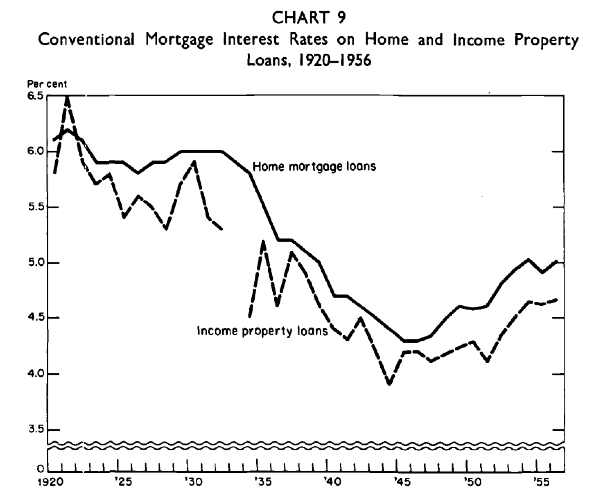

Historical Lozeni Prices at the beginning of the 20th century

While difficult to compare apples to an apple of mortgage prices before 30 years of renovated, National Bureau of Economic Chart Survey has a define in 1920 to 1956.

Since about 1920 until 1934, the normal mortgage prices are closed near 6%, and then rejected a low less than 4,5% point.

This is probably a media point used when they said the rates had never been a low thing in 60 years (back when they dropped early in 2010s).

The average tax rates in 1920s to 1950s

- We see a strong decrease in seed prices from about 1935 to 1945

- And then down a few years before the prices begin the maximum increase as 18% in the early 19800s

- Perhaps because of World War I II ended and all government’s bills associated with inflation

- Raised a second cycle of inflation related to Embargo of Embargo’s Embargo

However, it was not clear what forms of the girlfriend were over the most, and at the preparation of 30 years, it was actually a standard. But it provides a small context.

The good news is because the 3% tax rates are at the beginning of 2020s, maybe we can look at those who are very low in the 20th century text.

If only in Freddie Mac’s details since 1971, 30 years were scheduled 7.75% At that time.

But that includes some of the highest years in the 1970s and 1980 and other lowest years in 2010s and 2020.

Many like to refer to modern prices as a normal mortgage, but that does not mean that they are not much higher than they were supposed to.

In fact, they nearly again turned off to 2021 to 2023, from 2075% to 8%, ordinary is the highest quality time.

Since 1990, 30 years were prepared at 6% near 6%, thanks for part of the lower lower prices visible ten years ago.

So maybe the ranking prices are closest to its long-term moderation today in HIGH-6S. But without the help of domestic prices and / or higher wage, money available will remain lowly low, which is why home sales has disclosed.

Before creating this site, I worked as an account official because of the seller of the sales asset in Los Angeles. My first experience of 2000s encouraged me to start writing about 19 years ago to help the consumers that would be better and better. Follow me on X by taking hot.

Source link

.png?w=390&resize=390,220&ssl=1 "Introduction: Why Commercial Lending Will Look Different Towards 2026")