It’s been a great year so far for mortgage rates, which are up nearly 8% over the past year.

The fixed 30-year is now priced at a full 1 percent below last year’s levels, according to Freddie Mac.

And if you consider the 7.79% rise seen in October 2023, it is now less than 150 points.

But the recent mortgage rate rally may still have gas in the tank, especially with the way the mortgage market has held together in recent years.

Just getting spreads back to normal could result in another 50 basis points (.50%) or more of loan-rate relief going forward.

Forget The Fed, Focus On Spreading

There are several reasons why mortgage rates have improved over the past 11 months.

For one thing, the 10-year Treasury yield has fallen due to the sluggish economy, which is a boost for bonds.

When the demand for bonds increases, their price increases and their yield (interest rate) decreases.

Long-term mortgage rates follow the 10-year yield index because they have the same maturity (loans are typically prepaid over ten years).

So if you want to track mortgage rates, the 10-year yield is a good place to start.

However, inflation has fallen significantly in recent months due to monetary tightening from the Fed.

They have raised prices 11 times since the start of 2022, which seemed to finally do the trick.

This has pushed the 10-year yield down from around 5% in late October to around 3.65% today. That alone can explain a good part of the level of mortgages seen since then.

But there has also been some reduction in the “spread,” which is the MBS investors demand for the risk premium associated with a mortgage versus a government bond.

Remember, mortgages can fall into distribution or be prepaid at any time, while government bonds are a sure thing.

So buyers pay a mortgage premium relative to what that bond might be trading for. Typically, this spread is about 170 basis points above the 10-year yield.

In other words, if the 10-year is 4%, the 30-year fixed may be offered at about 5.75%. Recently, credit spreads have widened due to increased volatility and uncertainty.

In fact, the spread between the 10- and 30-year fixed rates was nearly double the long-term average, meaning homeowners were stuck with 3%+ more.

For example, where the 10-year was around 5%, the 30-year fixed rate was priced at around 8%.

Normal Distributions Can Reduce Rates by Another 60 Basis Points

A new commentary from JP Morgan Economic Research asserts that “prime rates could fall by as much as 60 bps over the next year” due to spread normalization alone.

And even more so if the market rates further Fed rate cuts.

They note that the primary/secondary spread — what a homeowner pays compared to the value of a secondary mortgage (what mortgage-backed securities trade for in the secondary market) remains wide.

Head of MBS Research Agency at JP Morgan Nick Maciunas said if the yield curve steepens and falls again, mortgage rates could drop another 20 bps (0.20%).

In addition, if the prepayment risk and term adjustment return according to its norms, the spread may compress another 20 to 30 bps.

Together, Maciunas says mortgage rates could improve another 60 points (0.60%).

Assuming the 30-year fixed rate was around 6.35% when that study was released, the 30-year could drop to 5.75%.

But wait, there’s more. Without the mortgage market simply rebalancing itself, further rate cuts by the Fed (due to the ongoing recession) could drive rates even lower.

How Much Will the Fed Really Cut Next Year?

Remember, the Fed does not set loan rates, but takes cues from economic data.

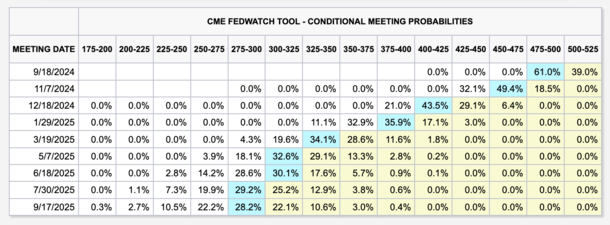

At a glance, the CME FedWatch tool has the fed funds rate in a range of 2.75% to 3.00% by September 2025.

That’s 250 bps below current rates, of course others “price in between” and the other is not. There’s still a chance the Fed won’t cut that much.

However, if it becomes more clear that rates are actually too high and will decline to those levels, the 10-year yield should continue to decline.

If we combine the low 10-year yield with tight spreads, we could see a 30-year fixed in the bottom 5 or even the top 4 next year.

After all, if the 10-year yield drops to around 3% and spreads return to near normal, if they’re too high, you start to see a fixed 30-year dip below 5%.

Those paying discount points at those rates may have a chance to go even lower, perhaps in the mid 4s and maybe, just maybe, something in the high 3s depending on the nature of the loan.

Note that this is all subjective and subject to change at any time. Similar to rising housing prices, there will be unexpected bumps and turns along the way.

Before creating this site, I worked as an account manager for a real estate broker in Los Angeles. My experiences in the early 2000s inspired me to start writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the mortgage process. Follow me on Twitter for the latest.

Source link

.png?w=390&resize=390,220&ssl=1 "Introduction: Why Commercial Lending Will Look Different Towards 2026")