Lately, there has been a lot of speculation surrounding the direction of mortgage rates.

I’ve been involved in this for a bit as I’ve tried to figure out what’s going on with the rates.

Despite recent increases over the last 30 years ranging from about 6% to 7%, I maintain that they remain in a downward trend.

Actually, I haven’t changed my opinion since they started to fall about a year ago when they seemed to be coming off an 8% lead.

Many other economists and pundits have been mixed since the Fed began cutting rates in September, but that may be wrong.

Mortgage rates tend to drop before down payments

The first Fed rate cut in this cycle took place on September 18, and the Federal Reserve chose a 50 basis point reduction to the federal funds rate (FFR).

This marked a “pivot” after the Fed raised rates 11 times since early 2022 to fight inflation.

The reason they ended up running for office after the inflation rate was so high was because they felt that inflation was no longer their main concern, and that keeping prices high for a long time could hurt employment.

Their dual mandate is price stability and sustainable high employment, which may be difficult if fiscal policy remains too restrictive.

However, that led to a reduction in their initial rate and to everyone’s surprise, the 30-year flat rate has risen almost a full percentage point since, as seen in the chart from MND above.

Many people believe that the Fed controls mortgage rates, so that when they “cut,” mortgage rates also go down.

This is a longstanding myth that has proven difficult to shake, but perhaps the latest move in mortgage rates will finally put it to bed.

After all, the 30-year fixed was around 6.125% on September 18th, and quickly rose to 7.125% in early November.

So maybe people will stop believing that the Fed controls mortgage rates.

However, loan rates tend to move in the same direction as the federal funds rate.

Why? Because while the FFR is a short-term measure, and the 30-year fixed rate is obviously a long-term rate, the Fed’s rate cuts often indicate economic weakness ahead.

And weakness means a flight to safety, aka investing in bonds, which increases their price and lowers their yield (interest rate).

Mortgage Rates Respond Appropriately to Fed Rate Pivot

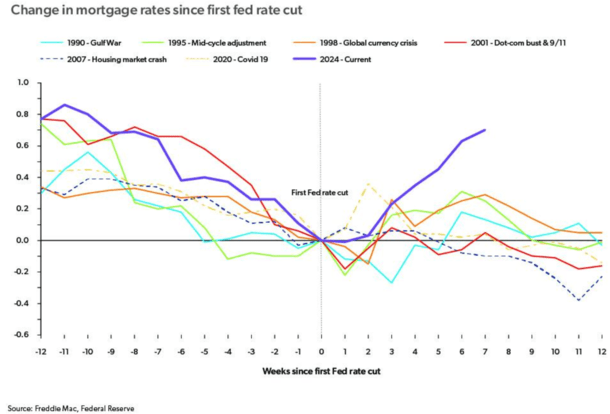

Check out this chart from Freddie Mac, which details mortgage rate movements in the 12 weeks before and 12 weeks after the first Fed rate cut.

While 2024 appears to be out of the question, when you consider that rates fell by around 80 bps leading up to the cut, the rebound was completely unexpected.

Because so much is baked into Fed cuts, rates tend to jump slightly once the news is delivered. It’s a classic buy a rumor, sell a news event.

Also consider that the strong jobs report was released shortly after the Fed’s policy decision, which had a significant impact on prices.

So it also depends on what happened to happen at the same time. What if that jobs report was weaker than expected? Where would we be today?

However, there are instances in the past when mortgage rates followed a similar pattern, including 2020 and 1998.

In most years with a pivot, mortgage rates rise for a short period of time before starting to fall again.

But most importantly, mortgage rates keep falling leading up to the pivot. There was always a pre-pivot drop.

Simply put, mortgage rates favor expectations of the Fed’s pivot, which explains why again this year the 30-year fixed rate fell from 7.5% in May to 6.125% in September.

Will Mortgage Rates Return to the Way They Did in the Past?

Using the chart above, we can see that the 30 year fixed rate remains significantly higher than the pre-Fed rate cut.

But in the last few weeks (captured in the first chart), the prices have gone down a bit. The 30-year rose to around 7.125% and fell to around 6.875%.

So it gained about 25 basis points to its upside and may be set to gain more.

It will be about 12 weeks from the Fed pivot in two weeks from now, so we are running out of time to get it all back.

However, history shows that mortgage rates tend to return to their pre-Fed rate cut levels in just three months.

And often even lower than that, if other pivots seen in the past are any indication.

It doesn’t mean that history always repeats itself, but it would be surprising if rates don’t return to the low 6% range and soon, even match the levels seen in mid-September.

It also wouldn’t be alarming if they went lower or even higher over time, possibly in the upper 5% range and more.

And, if you look at the chart, they usually keep falling. But everything will depend on economic data releases, including the all-important jobs report on Friday.

Making things murkier is the incoming administration and their programs, which have put prices on a bit of a rollercoaster, and which may explain why they have risen so much lately.

Read on: What will happen to housing prices under Trump’s second term?

Before creating this site, I worked as an account manager for a real estate broker in Los Angeles. My experiences in the early 2000s inspired me to start writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the mortgage process. Follow me on Twitter for the latest.

Source link

.png?w=390&resize=390,220&ssl=1 "Introduction: Why Commercial Lending Will Look Different Towards 2026")