I’m bald. December is a “hard time” for me. I lose them often. I depend on them like appendages. After a few frantic minutes of searching as I head out the door, I finally succumb to my embarrassment to find one right there in my coat pocket, patiently waiting.

An idea would be like this. It is there, but we have lost it. We had it, but now it has disappeared, leaving only fear. Invariably, we can even create fake news. “I bet Ashley put it somewhere!”

In our world of short attention spans, it’s easy to lose sight of loan amounts. Like a shopping cart with a bad wheel, we have a natural tendency to pull our expectations into an area that may not follow reality. As a pilot, you are taught to trust your instruments, not your instincts. With financial matters, we should trust the data, not the gut.

In that vein: What’s the Rest of the Mortgage Rate? Where should we target our expectations for the general trend in mortgage interest rates?

A common comment from home buyers is what I will call “The Refinance Refrain.” The refrain finds its voice when the client chooses to pay a negative long-term rate because he plans to repay the money. when rates will return next year. I heard a strong chorus of The Refinance Refrain from mid-2022. Hey, maybe I sang a few bars myself.

In context, an interest rate with no points is higher than one where the consumer pays the equivalent of discount points. If you plan to hold your mortgage for a long time (usually 3.5 to 4 years or more), it is better to pay a certain number of discount points and get your money back over the loan term. If you believe that you will hold the loan for a short period of time, save your money and take a high/no credit rating on your short term financial instrument.

Below is a chart of the 30-year mortgage rate since 1971.

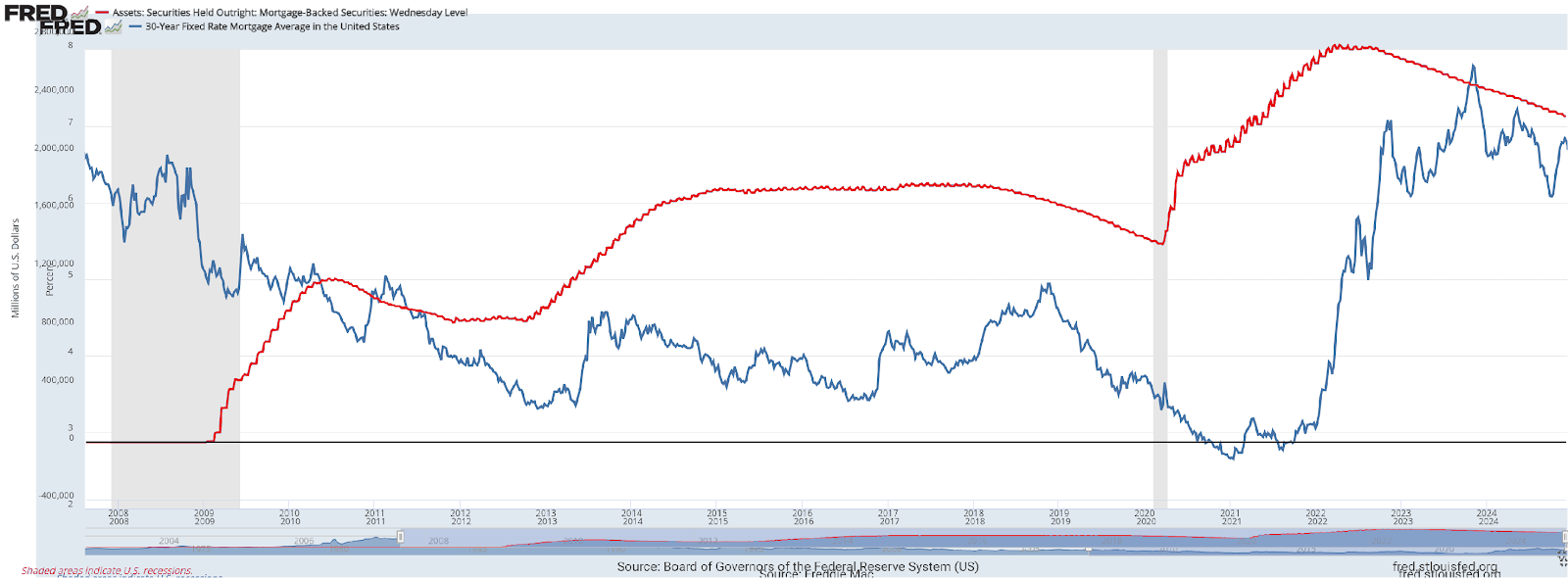

And here’s the same chart zoomed in from 2008 to the present:

You’ll note that the 30-year fixed rate dipped below 5% for the first time in modern history in 2009, almost 16 years ago. Why? What magic economic lever was pulled to force prices down and increase the affordability of home ownership in the suburbs?

A business partner can tell you it’s because the Steelers won the Super Bowl in 2009, the last game to feature legendary commentator John Madden. Scholars still debate this spontaneity.

Truth be told, the reason mortgage rates have dipped below the 5% Mendoza line is because of the actions of our Federal Reserve. In 2008, Bear Stearns and Lehman Brothers sat down for the results banquet. But the great tragedy was still going on. US Treasury Secretary Hank Paulson said “we are facing the most difficult and unpredictable financial crisis of any lifetime.”

“Too big to fail” was upon us.

In December 2008, Fed Chairman Ben Bernanke, a student of The Great Depression and a toboggan aficionado, had taken immediate action with the Federal Reserve Board to reduce the Fed Funds Rate to 0%-0.25%. Still, Bernanke knew that this contagion required a stronger response than a short-term reduction in borrowing costs. Bernanke needed the long end of the yield curve to follow. How can one control the long end of the curve?

In January 2009, the Federal Reserve Bank of New York changed history forever by stepping aside and putting themselves in the game as the starting Quarterback of the Financial Crisis. The Fed was now the market participantbuying mortgage-backed securities for the first time. As Madden would say, “don’t worry about the horse being blind; just load the cart.”

The Fed has announced plans to buy $1.25 trillion in mortgage-backed securities (MBS), a move that should lower long-term interest rates, making borrowing cheaper to stimulate employment. They hoped that these actions would bring stability to the financial system by providing capital, which is the backbone of the modern economy.

Spoiler alert.

It worked.

Wow.

Philosopher Francis Bacon wrote “sometimes the cure is worse than the disease.” In case it is too big to fail, I will take the remedy. This disease would cripple, crush and cripple the United States economy. This was a time of “no milk on the shelves”, and I truly believe that history will judge Bernanke kindly. But Francis’s words are still heard. Medicines leave side effects.

The Fed’s actions were called “Quantitative Easing.” Leave it to economists to take something historical and make it sound like a laxative. Quantitative Easing 1 (QE1) ended in the spring of 2010. Before we could say our 2011 New Year’s resolutions, QE2 had already started. The Fed’s second round of stimulus included the purchase of $600 billion in US Treasury securities. This program will continue until mid-2011.

Like Brett Favre and retirement, sometimes we don’t know when to stop. In September 2012, the Fed committed to QE3, a $40 billion per month purchase program of mortgage-backed securities aimed at supporting the housing market. This round of deflation would last longer than others, until October 2014. From then to the pandemic, the Fed continued to reinvest payments from its holdings into new MBS. Not really a continuation of QE3 but no exit either. Think of it like microdosing in the stock market. Don’t steal that. It’s mine. I did it.

The Fed’s strong public statement of intentions to keep interest rates low is in line with their history of subjugating the securities market to lead another game-winning drive. Investors had nothing to fear. Delivered to the rescue. As the 1973 song by The Spinners goes, “whenever you call me, I’ll be there.”

Below that chart shows the 30-year default since 2008, overlaid with the Fed’s MBS purchases during the decade of the 2010s (red line). A grade below 5% occurred for the first time in 2009. The 2010 Mortgage Championship Dynasty was made possible by the actions of our star Quarterback, the Federal Reserve. Folks, this was not the rule, it was the exception. This Fed’s version of a mortgage was like Tom Brady for the Patriots. The Patriots have no natural claim to pedigree outside of Tom Brady. And mortgage rates don’t have the natural right to historic lows without their QB star, either.

QE has been replaced by QT (quantitative tightening), the antidiarrheal of economists. The Fed is no longer buying MBS and although inflation has been reduced, mortgage rates remain between 6.25-7.25%. Tom Brady retired. The Patriots are nursing again. Kings end. Here begs the question, what is the Mortgage Rate Resting State?

It’s been a long time since the Fed began to influence the housing market, it’s difficult to announce a secure, modern answer to this question. But I can tell you for sure, it is not less than 5%.

Back to Sir Francis Bacon and his cautionary tale: Since the Fed left the bench in 2009, it has been creating bubbles. And they still are. The extremely low levels of the pandemic have halted the domestic resale market. Hello, lock effect. Existing home sales will close 2024 at 1995 levels. We have heavily armed every generation of Americans since the homeowners.

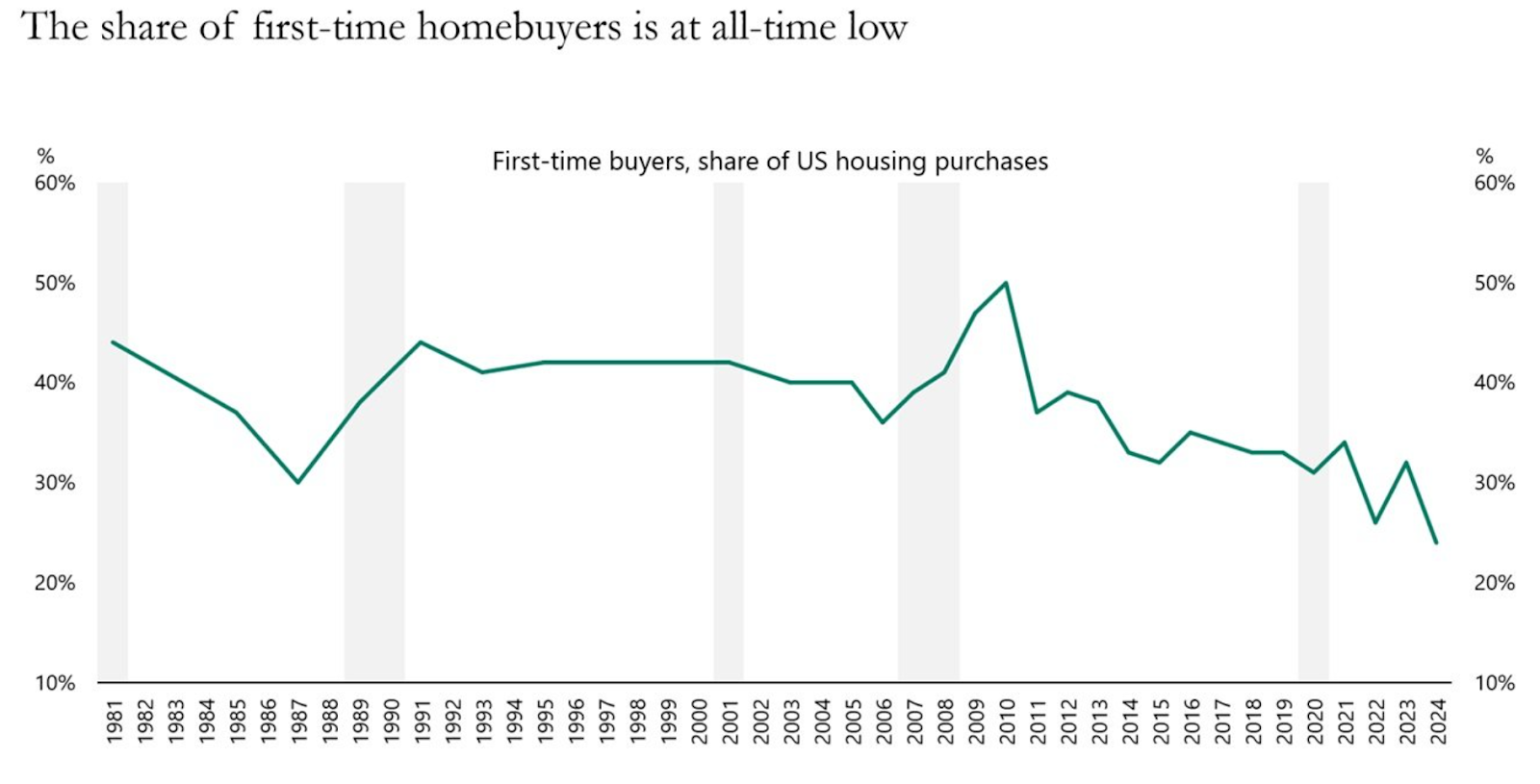

Today’s bubble is an on-demand bubble. First-time home buyers now make up only 24% of all home buyers, the lowest share since NAR began tracking this data (43 years). They take themselves out of the game.

The average age of home sellers was 63 this year, the highest on record. The median age of a first-time homeowner jumped to 38, up from 35 at the same time last year. In the 1980s, the average consumer was in their 20s. This bubble will have its own unique and dynamic consequences for lenders to deal with in the latter half of the 2020s.

Meanwhile, as mortgage professionals, we can do wrong to our clients if we promote narratives that have no basis in fact. The solution to any problem begins with the determination to bring it to light. To conclude with another Madden-ism: Coaches must look at those who don’t like to see and listen to those who don’t want to hear.

The advisor trumps the salesperson. Every time.

Mark Milam is the president and founder of Highland Mortgage.

This column does not necessarily reflect the opinion of HousingWire’s editorial department and its owners.

To contact the editor responsible for this piece: [email protected].

Related

Source link

")