If you haven’t heard about 30-year mortgage rates recently, maybe an ARM would be a better fit for you.

This is especially true if you don’t plan on staying at home for a very long time.

There are a variety of adjustable rate mortgages available to homeowners today, with fixed rate periods.

One of the abbreviations for hybrid-ARMs, which are fixed-rate mortgages before they can be modified, is the “3/1 ARM.”

Let’s learn more about how it works to see what a different alternative to a 30-year mortgage could be.

3/1 ARM Description

- It is a hybrid home loan scheme with a tenure of 30 years

- That is, it is fixed before it can be changed

- You get a fixed interest rate for the first 3 years

- Then it can adapt once a year for the remaining 27 years

As the name suggests, it is an adjustable rate loan that has two main components.

The first number (“3”) indicates the period during which the interest rate on the loan is adjusted. In this case, three years. This means that your prime interest rate will not change for 36 months.

This is good news if you’re afraid of a (high) rate adjustment, and it’s also useful if you only need short-term mortgage financing.

The second number (“1”) represents the maintenance frequency, which you may have guessed, is yearly. Of course, this means that the rate can change from year to year once the first three years are over.

For the record, the 3/1 ARM is still a 30-year loan, so you get a fixed rate for the first three years, and an adjustable rate for the remaining 27 years. This is why it is sometimes called a 3/27 ARM loan as well.

Once those three years are up, your interest rate will be adjusted based on the margin and an associated mortgage index, such as the SOFR.

This is known as the fully indexed rate (FIR), and is limited by caps, which mean how much the rate can increase or decrease initially, periodically, and over the life of the loan.

Let’s look at an example of a 3/1 ARM:

| $350,000 Loan Amount | 3/1 ARM | 30 years fixed |

| Mortgage Rate | 5.375% | 6.5% |

| Monthly P&I payment | $1,959.90 | $2,212.24 |

| Total Cost in 36 Months | $70,556.40 | $79,640.64 |

| Balance Remaining After 36 Months | $334,716.08 | $337,460.25 |

| Total Savings | $9,084.24 |

3/1 ARM Rate: 5.375% (first 36 months)

Margin: 2.5 (fixed for the life of the loan)

Index: 1 Year SOFR (5.25% variable)

Spelling: 2/2/5

Consider a 3-year ARM with an initial rate of 5.375%, limited to the first 36 months of the loan. During this time, you’ll save about $9,000 compared to a 30-year fixed rate at 6.5%.

You can also pay off a higher loan balance due to the lower interest rate offered.

But you also need to consider what happened in the remaining 27 years.

If the margin is 2.5 and the related mortgage index is 5.25%, your FIR can rise to 7.75%, assuming the caps allow such a move.

Using our example, the interest rate may adjust 2% above the original rate in its first adjustment, so an increase from 5.375% to 7.75% would not be allowed.

Instead, the rate could rise to 7.375%, but could rise again to 2% at the next adjustment 12 months later.

Obviously, this can be a big hit to the wallet, which is why many homeowners will look to sell their home or refinance their mortgage before then.

Unfortunately, loan rates may not be attractive during the three-year period after taking out your loan.

You may also not be eligible for financing if your credit score or income drops, or if the underwriting guidelines change over time. Falling home prices can also put your plans to refinance or sell on hold.

In short, you are taking a very high risk of getting a low interest rate for 36 months, so have a plan in place if and when rates rise.

3/1 ARM Home Rates

- 3/1 ARM rates can be much cheaper than a 30-year fixed

- But the rate difference will vary from bank/lender (some don’t offer big discount)

- Spreads between products can also widen or narrow over time depending on market conditions

- Shop around to find a lender willing to give you a 3/1 ARM at a low rate

Now let’s talk about the 3/1 ARM rates, as I have already referred to, which come in cheaper than the 30 year fixed rate mortgage.

The big question is how much cheaper, as the discounted rate will determine whether the 3/1 hybrid ARM is worth the risk.

After all, there are a number of risks involved when your mortgage rate is not set in stone. If it gets too high, you could face mortgage payment problems in the near future, and you could even lose your home if things get really bad.

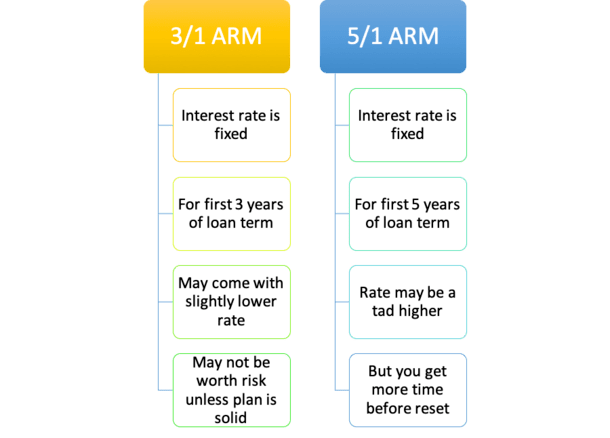

I looked a little closer to see how the 3/1 ARM rates stack up against the 30-year fixed and 5/1 ARM, which offers two additional years of fixed-rate security.

I’ve found that rates vary greatly, but can often be much cheaper than a 30-year fixed-rate loan.

For example, I recently saw 3/1 ARM rates advertised as low as 5.75%, while 30-year fixed rates were going for closer to 7%, with no mortgage points on either option.

Of course, I’ve seen tight spreads as well, with some 3/1 ARMs priced at 5.875% or 6%.

But you should expect an average discount of at least a percentage point, maybe more if you’re lucky considering the risk involved.

You qualify for a 3-year ARM It’s Wrong So You Might Want To Skip It

Another major challenge with a 3-year ARM is that the qualifying rate used is usually 5% above the value of the note.

Yes, you read that correctly. A perfect five percent is the highest score. In other words, if your rate is 5.375%, the lender will need to qualify you for a rate of 10.375%!

This is the rule employed by both Fannie Mae and Freddie Mac and followed by many other lenders, including credit unions. Maybe some don’t, but it’s good to think about this when buying an ARM.

Currently, qualifying for a 5/1 ARM is excellent for borrowers.

Lenders use the larger note amount and two percentage points or the fully indexed amount. So that might be a more reasonable rate of 7.375% in our example.

And because 3-year ARMs and 5-year ARMs are priced equally, it might make sense to skip the former altogether and get two more years of limited-rate goodness.

3/1 ARM vs. 5/1 ARM Prices

When comparing a 3/1 ARM to a 5/1 ARM, you may only be looking at an average discount of 0.125% to 0.25%, depending on the lender in question.

And the 3/1 ARM is not even offered by all mortgage lenders. In fact, Wells Fargo, Chase, and Quicken Loans don’t even advertise them, although they both freely offer the 5/1 ARM and the 7/1 ARM.

This does not mean they do not offer a 3/1 ARM, it is not listed as a loan option.

Ultimately, the 3/1 ARM and the 5/1 ARM are very similar, so banks and lenders often offer the 5/1 ARM instead, especially since it offers two more years of fixed rates.

Another reason it’s so common today is because of the Qualified Mortgage (QM) rule, which requires lenders to consider the highest interest rate that can apply within the first five years.

Because 3/1 ARMs will see their first adjustment after just three years, lenders should consider a fully indexed rate (margin + mortgage index), which may be much higher than the original rate.

As such, a borrower may have more difficulty qualifying for a 3/1 ARM due to DTI rate restrictions and the like.

In other words, lenders may avoid the home loan program altogether in favor of simpler types such as a 5/1 ARM.

If you are looking for a jumbo loan, you may have more luck getting this type of home loan as high net worth individuals generally prefer short-term financing.

These loans were actually very popular before the mortgage crisis of the early 2000s, but they are now very rare.

Finally, three years can come and go in the blink of an eye, which partly explains its low popularity.

Also See 3/6 ARM (Cousin of 3/1 ARM)

- Today it is common to see 3/6 ARM advertised as well

- It is also an adjustable and fixed loan for the first three years

- But it fixes it twice annually after the first 36 months of the loan term

- This means you have two repairs a year to worry about

Another common type of three-year ARM is “3/6 ARM,” which works very similar to the 3/1 ARM.

The only difference is that after the first three years, the loan amount changes slightly every year (twice a year).

So you get two repairs a year between 4-30 years. Every six months, there will be an adjustment.

This makes the 3/6 ARM more efficient, as you have to pay close attention to the corresponding ratio indicator.

It seems that mortgage lenders are opting for a six-month adjustment period over a 12-month adjustment a lot these days.

Don’t be surprised to find that they only offer a 3/6 ARM compared to a 3/1 ARM. But if you only keep it for the first three years or less, it won’t matter.

It may work for you if rates drop and your rate drops every six months instead of once a year. But don’t count on it!

And recently I found a 3/5 ARM advertised by the Navy Federal CU, which is fixed for the first three years, then fixed every five years. So year 4, year 9, year 16, and so on.

3/1 Advantages and Disadvantages of ARM

Good

- You can get a lower mortgage rate relative to other loan options

- The rate is limited to the first 3 years (36 months)

- This will allow you to save money and pay off your loan balance faster

- It can often remodel, sell your home, or pay off your mortgage before it’s repaired

Bad

- The interest rate will change after only 3 years

- Depending on the caps the rate can jump a lot

- It may be difficult to make high mortgage payments

- The rate may not be lowered enough to justify the risk of resetting the rate

- You may be stuck with the loan if you can’t refinance/sell/pay it forward

Before creating this site, I worked as an account manager for a real estate broker in Los Angeles. My experiences in the early 2000s inspired me to start writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the mortgage process. Follow me on Twitter for the latest.

Source link

.png?w=390&resize=390,220&ssl=1 "Introduction: Why Commercial Lending Will Look Different Towards 2026")