Home prices have remained strong over the past two months, even with higher mortgage rates and inventory data. Our weekly tracker data is created to look ahead of regular monthly reports like the Case Shiller and the current NAR home sales report, and what I’ve seen over the past few weeks has shocked me.

I want to show you how the data has changed with mortgage rates heading towards 6% so that the next time this happens, we have a better idea of what to expect in the housing market.

Deviation from data

I aim to determine what level of mortgage rates we need to shift the demand curve, which in turn shifts the price curve in housing data. I have long believed that it is rare in the US after 1996 to have a trend of selling a home under 4 million. We had a few months where we got below this level, but nothing too bad.

Back on Nov. 9, 2022, I show how housing prices have changed based on forward-looking data. This podcast video is a tutorial on how to track this and why people who are predicting the 2023 house price crash got it wrong because they don’t have models that work. To date, these principles are still in effect. Let’s take a look at what looks different today compared to two years ago.

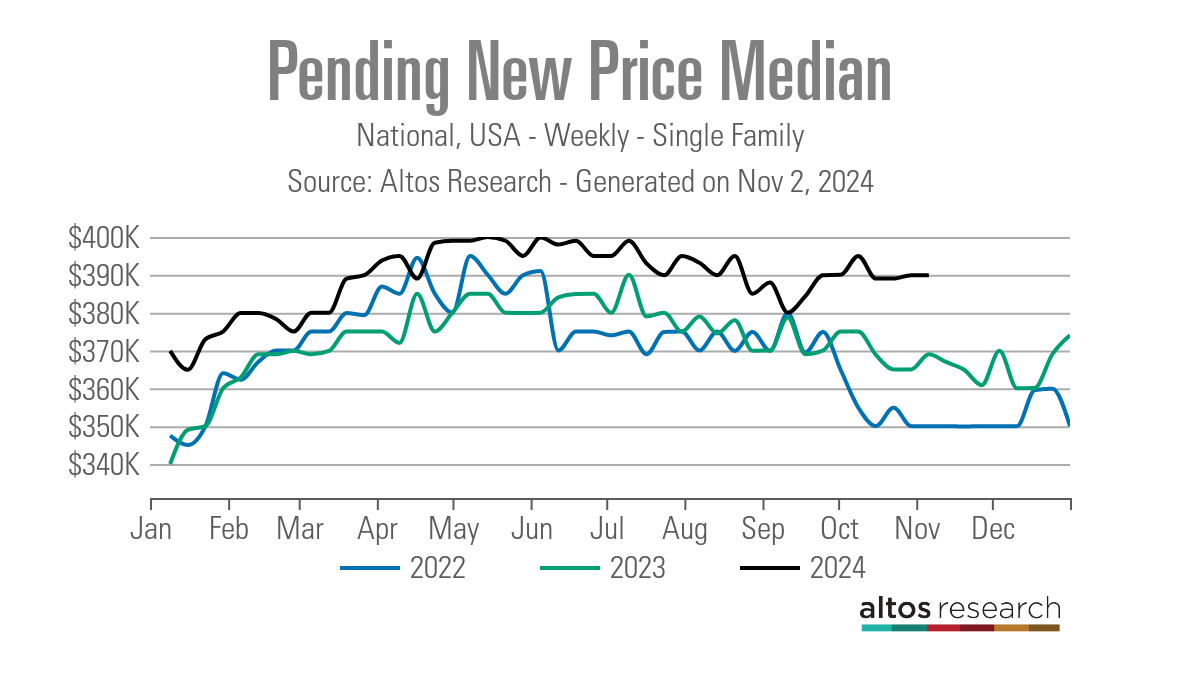

Pending contracts

First, we should note that we are in the third calendar year of the lowest home sales on record, once you adjust that number for employees. It’s not like we have underwater mortgages or tight credit – this was the biggest crash ever and sales are still down.

This means that we have a lower sales volume to work with because mortgage rates have been trending between 6%-8% for two years with rising prices, and we are not backing down from these levels. So, if we look at the contract data, the loan rates that went down towards 6% strengthened the data to the top and the data still shows a deviation from the levels that we see from 2022 and 2023. This means that lower sales get the company. a base on which to work.

My take on this is that we need a 6% loan to grow sales with some sustainability. It won’t be spectacular, but we can grow and keep sales at that level. We don’t need 3%, 4%, or 5% mortgage rates, but simply aiming for 6% and staying there can work.

If you want to see sales growth with some kick, you need cash prices below 6% over time, but since I can’t even predict those rates right now, I’m not going that way until the labor market breaks or spreads are available. much better. I just talked about this CNBC. This is something to consider in the future. Every year, wages rise, more homes are built and if mortgage rates fall, it should create another line of data for the required curve over 12 weeks. However, if mortgage rates can stay between 5.75%-6.25% for 12 months, they can maintain the high level of sales from the data we have seen since the end of 2022.

Buy app data

Last week, the purchase order data had a positive week-on-week print of 5% and was up 10% year-on-year. However, remember that October had a shallow bar, so take the whole month and show good year-over-year growth in context. If I took the entire month of October, which was good every week year-over-year, we had a growth rate of 7.4% over last year.

Let’s take a look at how this data line has performed so far this year.

While mortgage rates are rising at the beginning of the year (between 6.75%-7.50%), this is how the purchase application data looks like:

- 14 negative prints

- 2 flat prints

- 2 fine prints

With mortgage rates starting to drop in mid-June, here’s what the purchase requests look like:

- 12 fine prints

- 5 negative prints

- 1 flat print

- 3 positive positive growth prints year after year

As housing prices rise again, here’s where we are:

- 2 negative prints

- 1 fine print of the week

Here we can see a clear, forward-looking line of data with mortgage rates heading towards 6%, and now this makes two times since the end of 2022 this has happened when demand has improved for more than 12 weeks. I talked about the latest data separately on the HousingWire Daily podcast last week. But it is not only the demand but also the prices.

Price data

In terms of discounting data, many real estate experts take information from other sources and don’t know how to interpret it correctly. This was one of the funnest things to watch in 2024, by the way. They misread the percentage of price reductions and rising inventory data that mean national home prices should drop significantly this year. But we haven’t had a deep negative price curve data line this year, and it’s November now.

However, this year, mortgage rates are approaching 6%, making the amortization percentage data lower this year than the 2022 and 2023 data. Nothing too dramatic here, but as you can see from the pending contact data, we have rate variability that can change the data line even with rising housing prices.

There were several years of housing data in the early 1980s and mid-to-late 1990s, and from 2000 to 2005, where we saw an increase in inventory. again to sell. You can have rising inventory, increasing sales and rising prices. Percentage discount data is important if you know how to read it properly, and as you can see below, percentage discount data has dropped recently.

Shockingly, our average weekly new pending price data has strengthened even during a period of seasonally soft prices, especially now with higher inventory data. As you can see below, there is a noticeable deviation in the 2022 and 2023 data. This is why my forecast for 2024 is 2.33% and home price growth is at risk. If mortgage rates stayed close to 6%, you wouldn’t have to be a rocket scientist to guess what the data line was showing.

Weekly data lines

I focused on the deviation data in this weekend’s tracker, which is different than what we usually do; This is a quick look at the traditional data we display.

Weekly housing inventory is down slightly. This is a back-to-back week for a slight drop in inventory. We’ve seen good growth in active listing data this year, so for those who said that inventory won’t grow at high rates, 2024 hopefully changed your mind.

Inventory has fallen 736,014 to 735,718.

Data for new listings had a slight increase this week from 60,066 to 60,819.

The good news for 2024 so far is that inventory has grown. I wanted this to happen in 2023, but it happened too late to make a noticeable change. However, in 2024, we saw inventory growth and there is no new strong listing data from new listing data in 2024. To give you an idea of what the new highlighted listing looks like, compare 60,819 new listing data this week compared to the data we’ve seen this week over the years:

- 2009: 280,400

- 2010: 353,457

- 2011: 352,030

As I often say, we had different credit markets back then, so stop dancing with the ghost.

10-year yields and loan rates

My prediction for 2024 included:

- Loan rates range between 7.25% -5.75%

- 10-year yield range between 4.25%-3.21%

I will keep this as simple as possible. I’ve been talking about this 4.40% line in the sand on the 10-year yield for quite some time now. If this rate moves higher, we have broken the trend low in the 10-year yield that started on Oct. 16, 2023, while it was at 5%. There’s a lot going on this week, so let’s take a look. If you’re confused about the bond market’s action on Jobs Friday, this article goes into my take on that.

Mortgage spreads

Mortgage spreads had a good day on Friday, preventing prices from getting worse. However, the big story has been that spreads that have improved this year have been good for housing. If we had no progress this year, prices would not only be higher today but throughout the year. The spread has gotten worse recently but is still better than last year.

Next week: All bets are off

Between the election and Fed meetings this week, all bets are off on anything normal. I’ll be on the HousingWire Daily podcast three times this week to explain what’s happening. Monday’s podcast will try to explain what’s happening with the 10-year yield and mortgage rates.

This week, the 4.40% bond yield rate is key; closing above that level and getting a follow through bond sale can be problematic for real estate. However, try to ignore intraday movements—they can be wild around key technical levels. Good luck to everyone this week.

Related

Source link

")