Despite early concerns that interest rates would push mortgage rates up to 8% and reduce demand for housing, this week brought some encouraging news. The 10-year yield remained stable at a key technical level and even retreated, leading to an improvement in mortgage rates. Additionally, demand for housing has risen dramatically, even with higher mortgage rates.

Although the increase in demand may not be significant, it is still a positive development, and that should be celebrated! Let’s take a look at the latest housing data to get some insight into the market as we approach the end of the year.

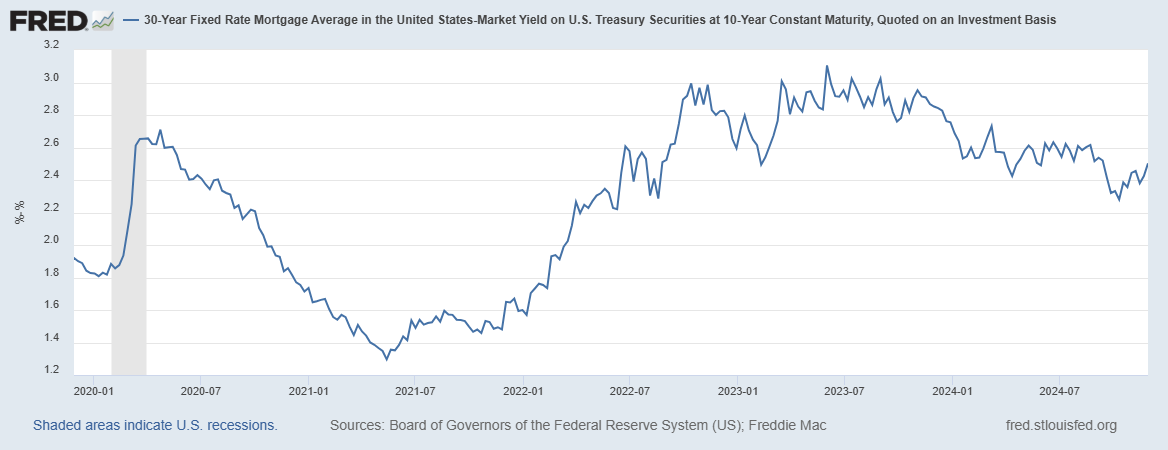

10-year yield and housing rates

My prediction for 2024 included:

- Loan rates range between 7.25% -5.75%

- 10-year yield range between 4.25%-3.21%

The recent drop in mortgage rates can be attributed to the volatility of the bond market and current sentiment among bond traders. They see the potential benefits of buying the 10-year bond at its current level, especially now that the Citigroup Economic Surprise Index has reached a short-term peak and is over.

Earlier, there was significant concern about the possibility of a new wave of inflation, which would require raising interest rates, which I threw cold water on in the latest HousingWire Daily podcast. However, the most recent peak in the 10-year yield was around 5% in 2023, and the decline to that level is still in place. Therefore, as long as the economic data does not surprise higher, bond yields should stay far from 5%, which means that loan rates will not be close to 8%.

When I talk about the Santa Clause meeting, I mean people who buy the 10-year yield and drive low mortgage rates, because of the slow dance between the 10-year yield and mortgage rates. This is what happened two years ago. We will see if we get a repeat this year.

Mortgage spreads

The mortgage spread situation improved in 2024, especially compared to the difficult times in 2023. As a result of this positive change, mortgage rates reached 6% with the 10-year yield reaching 3.37% by 2024. Imagine if spreads didn’t improve – loan rates would be over 7.50% right now!

Although we have seen a slight increase in spreads since mortgage rates started to rise in September, it is important to note that they are still in a much better place than the high rates we experienced last year. If spreads had remained as high as in 2023, mortgage rates today would be 0.60% higher. On the other hand, if we were looking at the average spread, we would see mortgage rates drop by about 0.93% to 1.03%. Overall, it’s encouraging to see progress in the mortgage market!

Weekly pending sales

Weekly pending contract data from Altos Research gives us an unusual view of real-time housing demand. It is interesting to see how this data follows seasonal trends, as shown in the chart below. Initially, we saw strong performance when loan rates were close to 6%. It is encouraging to see pending contracts holding up year over year, even though home prices and mortgage rates have been high recently. This trend has piqued my interest, and I’m happy to keep an eye on it! Imagine if mortgage rates suddenly stayed in the range of 5.75%-6.25% for 12 months.

Here are the weekly pending sales for the past few years:

- 2024: 317,080

- 2023: 296,615

- 2022: 299,312

While our pending contract data has shown year-over-year growth in recent months, NAR’s pending home sales have now stagnated.

Buy app data

The latest shopping app data was quite surprising. Whenever mortgage rates rise from trend lows, the results are negative for a period of time. However, last week’s app purchases data showed a 12% week-on-week growth, now bucking the trend for the past seven weeks, which wasn’t on my holiday bingo card. Last seven weeks:

While mortgage rates are rising at the beginning of the year (between 6.75%-7.50%), this is how the purchase application data looks like:

- 14 negative prints

- 2 flat prints

- 2 fine prints

When mortgage rates started to drop in mid-June, here’s what the purchase requests looked like:

- 12 fine prints

- 5 negative prints

- 1 flat print

With two years of data, we see a positive trend in the growth of purchase requests when loan rates approach 6%.

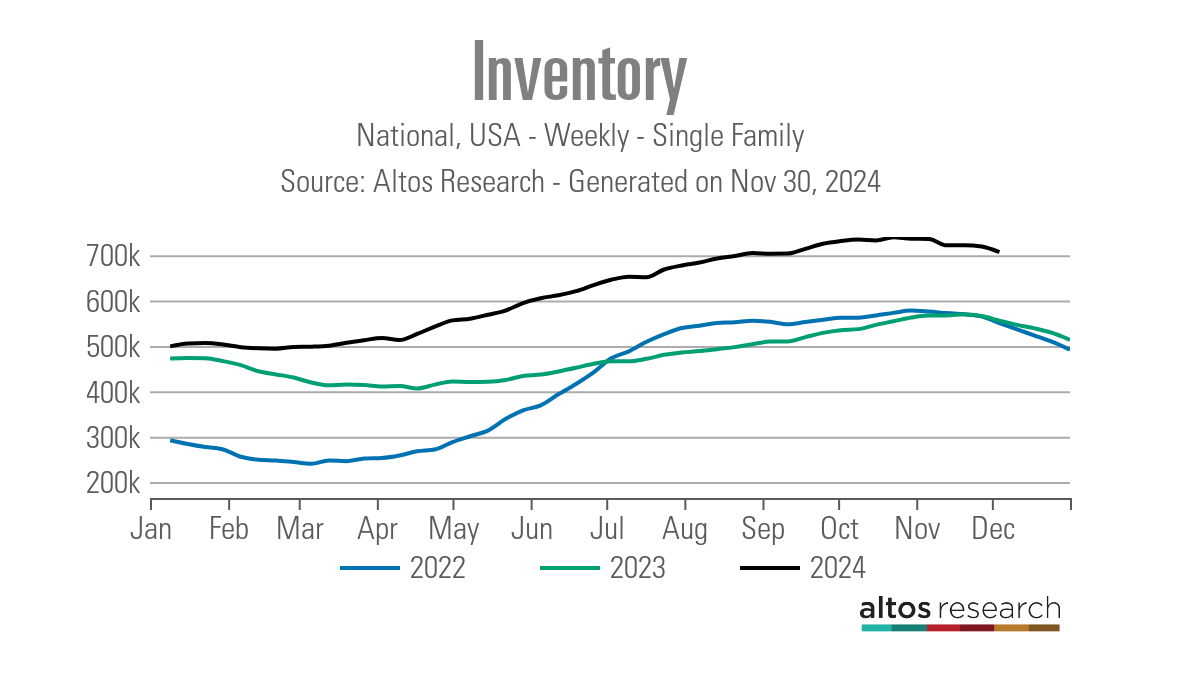

Weekly housing inventory data

Home inventory fell last week, which is normal for this time of year. We have to wait for the list to drop until the spring season starts to heat up again. The peak in inventory for 2024 will be 739,434, which is not a normal level of inventory, but at least we’ve seen good, healthy growth this year. Year-over-year inventory growth is the best housing story for 2024.

- Weekly inventory changes (Nov. 22-Nov. 29): Inventory decreased from 719,055 to 706,554

- In the same week last year (Nov. 24-Nov. 30): Inventory fell from 565,875 to 555,717

- The all-time inventory low was in 2022 240,497

- 2024 peak inventory so far 739,434

- In another context, the active listing for this week in 2015 was 1,082,020

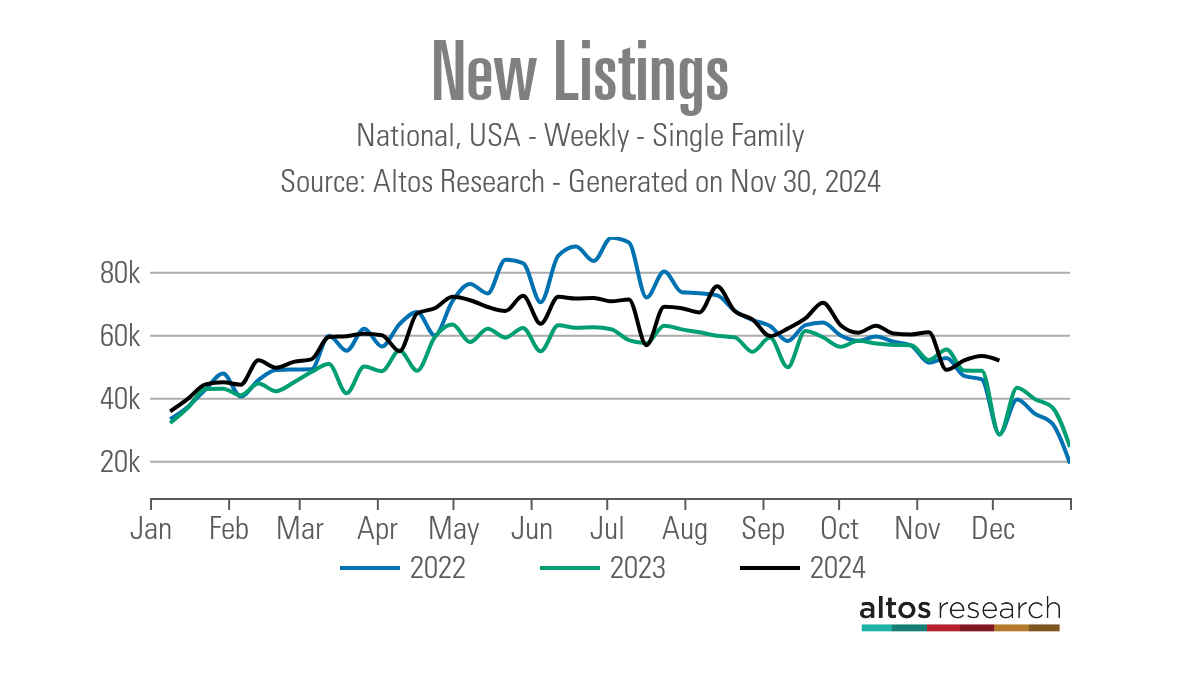

New listing data

Meanwhile, new listings data is experiencing a seasonal decline, with a slight decline seen last week. We can expect an even bigger drop of the season this week.

While I don’t underestimate the growth in new listing data during the peak 5,000 week season, it is encouraging to see growth in 2024. However, it is important to note that both 2023 and 2024 will be recorded as the two lowest years of new listings in history. . The idea that homeowners can rush to sell their homes in bulk is wrong. American homeowners don’t act like stock traders or get swept up in the sensational online content of YouTube the doomers. They just go about their normal life day by day.

New listing data for last week:

- 2024: 51,800

- 2023: 28,297

- 2022: 28,471

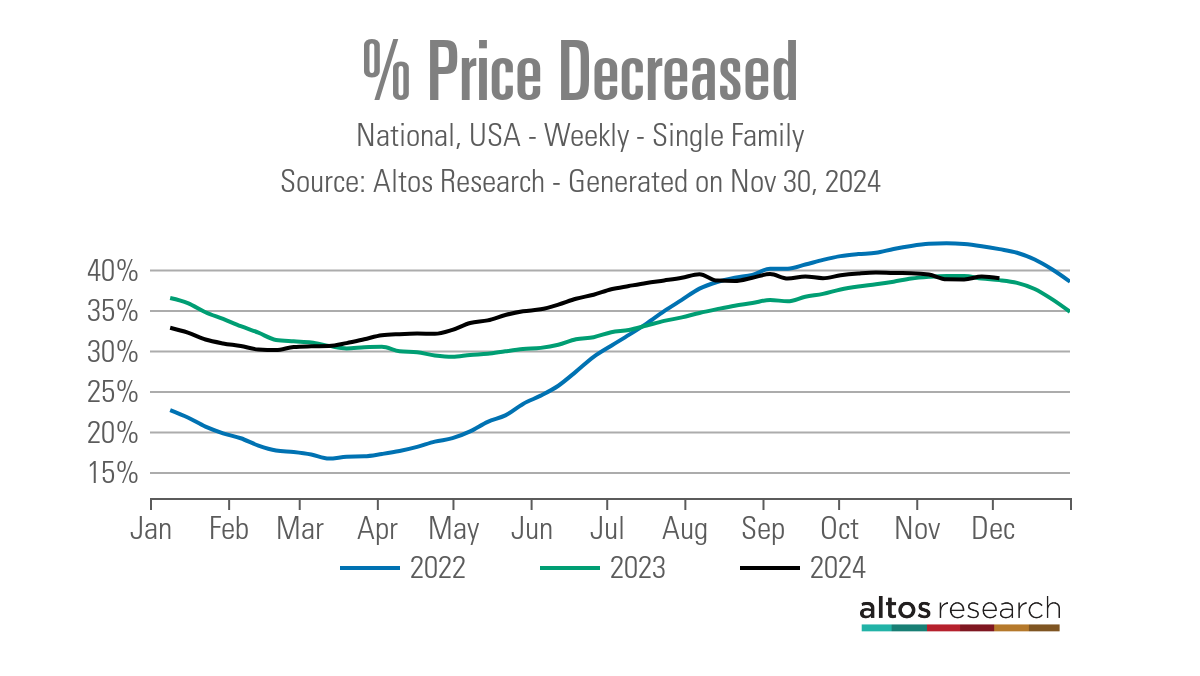

Discount percentages

In an average year, about one-third of all homes receive a price reduction, which is common in the housing market. When mortgage rates increase, the percentage of mortgages that reduce their rates tends to increase. Conversely, this trend can decrease when prices fall and demand rises, as we have seen recently when prices fall. However, mortgage rates have risen again. We are at the same levels as last year despite having more inventory available.

Here are last week’s price reduction percentages compared to previous years:

- 2024: 39.1%

- 2023: 39%

- 2022: 43%

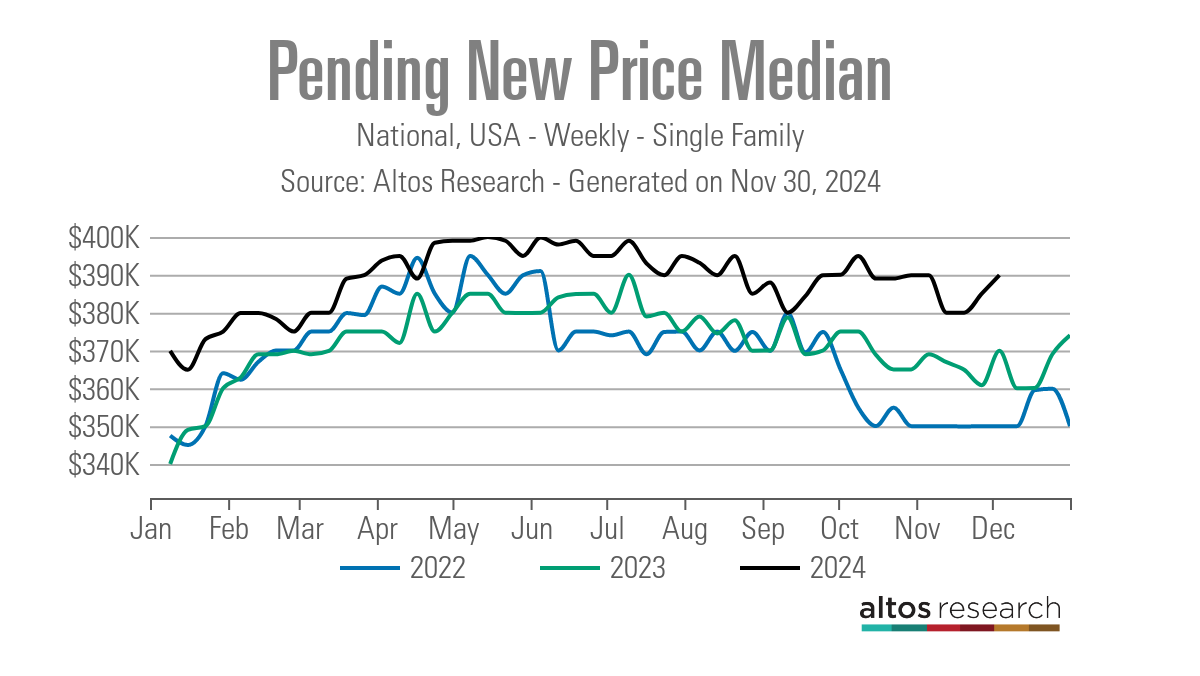

One thing that surprised me in the second half of 2024 was how strong our pending new house price index was in the mild season, with high property values and mortgage rates above 6%.

Next week: Jobs week!

There’s a lot to talk about this week — it’s the most important week of the month for economic data because it’s jobs week! We have several key reports, including job openings, the ADP report, jobless claims, and the key BLS Jobs report scheduled for Friday. We have already seen a significant drop in yields, so it will be interesting to see what happens next with mortgage rates. We also have ISM data, bond sales, and some Fed presidents speaking. So buckle up and let’s see how the bond market reacts to this week’s data.

Related

Source link

")