“What can I do with dollar?” Many people do not think that dollar is worth all these days, but that doesn’t mean it is worthless. In fact, there are many things you can do about the $ 1 bill that is not connected with making money for spending (and other many things you do). Some are interesting. Some are tricks. Some are surprising while others are just good things. If you have a $ 1 debt in your pocket and you want something interesting to do so, here are many ways you can use it may not be talking previously.

Use it as a bookmark

Pictures on FelipjcontrerasOne of the most obvious and simple things as a bookmark. You can do this using it as is, or you can find a small scale and create Origami Dollar Billmark. Any way, you will know exactly where to leave the next time you take your book.

Here is a wonderful letter of how to build Dollar Bill Origami if you are so inclined.

Compile

Wait … what? Why would you want to combine the bill? In true science! Dollar bills are made of ink with iron to help prevent resistance. If you include a dollar bill well, you can use the strong neodymium Magnet to separate the device without ink. Here is a lesson for doing this test. This is a wonderful work that you can do with, because, seriously, he would not want to combine the dollar?

Wait … what? Why would you want to combine the bill? In true science! Dollar bills are made of ink with iron to help prevent resistance. If you include a dollar bill well, you can use the strong neodymium Magnet to separate the device without ink. Here is a lesson for doing this test. This is a wonderful work that you can do with, because, seriously, he would not want to combine the dollar?

Infidel

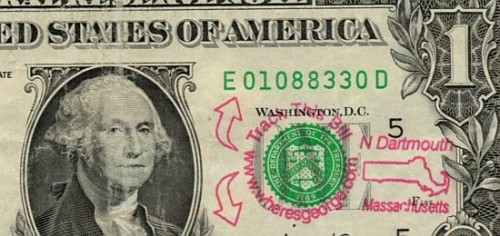

Have you ever wondered if your dollar is in your hand? Can you find in the database where George?. If someone else includes the serial number of the active bill, you see where it is before. If no one is to you, you can add and follow where it ends up to the next time others place it.

Have you ever wondered if your dollar is in your hand? Can you find in the database where George?. If someone else includes the serial number of the active bill, you see where it is before. If no one is to you, you can add and follow where it ends up to the next time others place it.

Find the owl

Many people believe that there is a hidden owl on the dollar bill. Take a moment to try to get it yourself. If you can’t, you may want to remove microscope to see if you can see you better that way. Then you can let the debate start if you don’t think that owl or not.

Many people believe that there is a hidden owl on the dollar bill. Take a moment to try to get it yourself. If you can’t, you may want to remove microscope to see if you can see you better that way. Then you can let the debate start if you don’t think that owl or not.

Burn!

While you can literally burn the dollar, the best way to burn is a mixture of water and rubbing alcohol. Doing this will make the diarrhea appear to be burning, but eventually the bill finally will remain strong to use other things. This delicious test is to do with children and is a good science test.

While you can literally burn the dollar, the best way to burn is a mixture of water and rubbing alcohol. Doing this will make the diarrhea appear to be burning, but eventually the bill finally will remain strong to use other things. This delicious test is to do with children and is a good science test.

Exchanging with a dollar coin

As dollars coins are not used in daily financial transactions, they seem special, especially for children. If you plan to give your child money, why not do it in coins rather than debt. This works very well when you give money through tooth or other special event.

As dollars coins are not used in daily financial transactions, they seem special, especially for children. If you plan to give your child money, why not do it in coins rather than debt. This works very well when you give money through tooth or other special event.

Make a ring

This is another wonderful job you can do. By little folding, you can turn your dollar into the ring. It takes a little origami skill to achieve this, but it is a good child’s project and will have a wonderful time wearing a new ring.

This is another wonderful job you can do. By little folding, you can turn your dollar into the ring. It takes a little origami skill to achieve this, but it is a good child’s project and will have a wonderful time wearing a new ring.

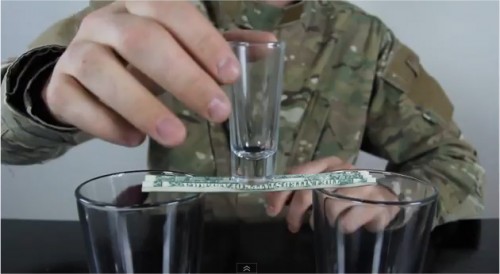

They balanced a glass that shot to

This is another good tactic you can do to win the betting of bar, or children can use their friends. While for example here we have two beer mirrors and a shot glass, you can use some different mirrors. The challenge is to ask your friends to set a dollar in all two glasses and measure a glass shot over it. It will seem impossible when they try, but then you can do it by rolling the dollar Accomion style to enable us. Watch the video below to see how.

This is another good tactic you can do to win the betting of bar, or children can use their friends. While for example here we have two beer mirrors and a shot glass, you can use some different mirrors. The challenge is to ask your friends to set a dollar in all two glasses and measure a glass shot over it. It will seem impossible when they try, but then you can do it by rolling the dollar Accomion style to enable us. Watch the video below to see how.

Get your birthday

There are many people who collect dollar bills finding interest. One of the popular types find those in your birthday within the serial number. For example, if you were born in 1985, you would want the bill to be a 1985 “somewhere inside the serial number. If you find a birth bishop of your year, you can save it as part of a collection or sell as people often pay the billing costs in eBay because many look at them.

There are many people who collect dollar bills finding interest. One of the popular types find those in your birthday within the serial number. For example, if you were born in 1985, you would want the bill to be a 1985 “somewhere inside the serial number. If you find a birth bishop of your year, you can save it as part of a collection or sell as people often pay the billing costs in eBay because many look at them.

Learn a really cool magic trick

If you have a $ 1 bill, play card and a pen, you can fill the wonderful magic trick that will surprise your friends and family. Although the trick will look amazing, it is not really difficult to do that. It is a beautiful island to be in your pocket where you want to make a vision. Skip to 4:11 to get to it.

If you have a $ 1 bill, play card and a pen, you can fill the wonderful magic trick that will surprise your friends and family. Although the trick will look amazing, it is not really difficult to do that. It is a beautiful island to be in your pocket where you want to make a vision. Skip to 4:11 to get to it.

Exchange 100 pans

If you want a long-lasting fun, you can take your dollar and then exchange 100 pens. There are many fun and exciting things you can do with pens. You can also look at all pens to see if you are lucky enough to find more elderly.

If you want a long-lasting fun, you can take your dollar and then exchange 100 pens. There are many fun and exciting things you can do with pens. You can also look at all pens to see if you are lucky enough to find more elderly.

Read the ideas of conspiracy

There are many Contributes around the $ 1 bill and the mark. Take one from your bag or bag, and follow 45 minutes (yes, you learn at that time) to listen to all sovereignty others who believe in Dollar Bill:

Find out where it is printed

You can view the payment you have and decide where it is printed. The book with dark brave before the bill focus on the left side indicates the Federal Bank commanding the bill. Here is anointing where your bill is listed:

You can view the payment you have and decide where it is printed. The book with dark brave before the bill focus on the left side indicates the Federal Bank commanding the bill. Here is anointing where your bill is listed:

A = Boston

B = New York City

C = Philadelphia

D = Cleveland

E = Richmond, Virginia

F = Atlanta

G = Chicago

H = st. Louis

I = minneapolis

J = Kansas City

K = Dallas

L = San Francisco

Spend

Scroll without your local dollar store and see what you can find there. While there are certain things that you never want but in the dollar shop, there are some practical things to come there. As the sale of these shops can always change, you may reach the appropriate GEM for your $ 1 in your hand.

Scroll without your local dollar store and see what you can find there. While there are certain things that you never want but in the dollar shop, there are some practical things to come there. As the sale of these shops can always change, you may reach the appropriate GEM for your $ 1 in your hand.

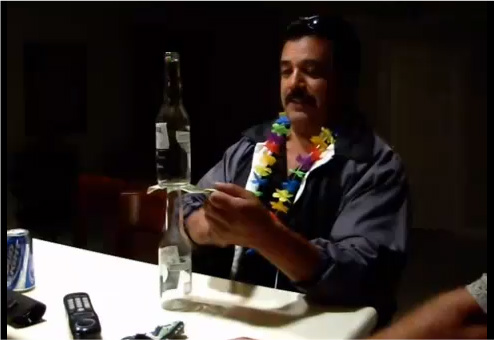

Open Coke bottle or beer

If you are in a party or want to please your friends, you can open a bottle of beer or a bottle of coke in the dollar. Yes, you read that well. By folding a strong bill, you can include a cap off in any bottle. So in the future there is another place and nothing open for the bottle, drilling $ 1 without your bag and makes all your friends happy.

If you are in a party or want to please your friends, you can open a bottle of beer or a bottle of coke in the dollar. Yes, you read that well. By folding a strong bill, you can include a cap off in any bottle. So in the future there is another place and nothing open for the bottle, drilling $ 1 without your bag and makes all your friends happy.

Find the star

Another cool thing to look at $ 1 bill is a star in serial number. Once a barrack number with the star at the end of it, this means that there was a print error during the production and the bill needed to print. This is called replacement notes. But they are often referred to as “the stars of the star”. This is a large bill you can collect, or can sell it more than a Face Face Face Auctions because most people like to collect these.

Another cool thing to look at $ 1 bill is a star in serial number. Once a barrack number with the star at the end of it, this means that there was a print error during the production and the bill needed to print. This is called replacement notes. But they are often referred to as “the stars of the star”. This is a large bill you can collect, or can sell it more than a Face Face Face Auctions because most people like to collect these.

HAVE HAVE A WORK ACT

If you walk down the road and hear the fun music that sounds the day, think about giving a dollar to the road musician. My philosophy is that if there is any street manufacturer who does something that is interesting enough to stand and watch ten minutes. The street seller will appreciate the action.

If you walk down the road and hear the fun music that sounds the day, think about giving a dollar to the road musician. My philosophy is that if there is any street manufacturer who does something that is interesting enough to stand and watch ten minutes. The street seller will appreciate the action.

They match the coin

This one takes little habit, but it is fun when it is down. The challenge of your friends to estimate the coin on the side of $ 1. When they don’t, you can show them how they did this bill in half and open it slowly about the coin.

This one takes little habit, but it is fun when it is down. The challenge of your friends to estimate the coin on the side of $ 1. When they don’t, you can show them how they did this bill in half and open it slowly about the coin.

Conceal

Hide dollar pay in a particular place where one will find it, and where he does it will bring little happiness in their day. I have a few favorite books for everything famous. When I go to libraries libraries, I would like to get a book and hit dollar to surprise the next reader. There are thousands of places that you can set a dollar that illuminated the person’s day when they got it.

Hide dollar pay in a particular place where one will find it, and where he does it will bring little happiness in their day. I have a few favorite books for everything famous. When I go to libraries libraries, I would like to get a book and hit dollar to surprise the next reader. There are thousands of places that you can set a dollar that illuminated the person’s day when they got it.

Pull down under the bottle

Here is another tactic you can use to earn money (or just cheat your friends). They challenged the removal of the payment from under the top bottle of beer (or POP) without touching the bottle and not having a bottle of bottle. They will probably try to drag the bill from under the trial of the bill immediately, but they will find that doing this will knock at all times. Instead, you will gradually release a dollar and win the bet (surprise your friends).

Leave the bar

There seems to be a growing number of barriers that encourage their fossils to wear dollar debts on the walls and the bhard of the bar. When you visit one of these bars (or you can start a new tendency to your local bar), you can write your name on the dollar bill and paste it on the wall.

There seems to be a growing number of barriers that encourage their fossils to wear dollar debts on the walls and the bhard of the bar. When you visit one of these bars (or you can start a new tendency to your local bar), you can write your name on the dollar bill and paste it on the wall.

Pull between two bottles

This is another beautiful trick you can do with any $ 1 money you have when you’re in line. Take a bill and set between two bottles (this bottle is high down the center of the middle, but can do above the bottle at the top bottle). Ask you friend to try to get this law without touching bottles. They will try to pull the bottle on the side that will fall. Then you can do it effectively with a small plan.

This is another beautiful trick you can do with any $ 1 money you have when you’re in line. Take a bill and set between two bottles (this bottle is high down the center of the middle, but can do above the bottle at the top bottle). Ask you friend to try to get this law without touching bottles. They will try to pull the bottle on the side that will fall. Then you can do it effectively with a small plan.

Make a paper plane

Pictures of jarednoel helpTake your money and make a paper flight on it. The easiest thing can be to make the type of paper that performs a standard paperwork. You don’t have to stand there. You can also do F-14 Jet Fighter if you really want to challenge yourself.

Challenge your friend to hold it

This is the Oldie person, but Hadeie. The challenge for your friends is to try and hold the dollar before falling into their hands. You hold it while putting their hand around them (without touching) and when throwing it, they tried to shoot their hand soon enough to catch it. Only laws are not able to close their hand before seeing it drops and cannot move their hand to help hold. The reaction of their brains that you see is thrown to close their hand long enough that the bill will not take hold.

This is the Oldie person, but Hadeie. The challenge for your friends is to try and hold the dollar before falling into their hands. You hold it while putting their hand around them (without touching) and when throwing it, they tried to shoot their hand soon enough to catch it. Only laws are not able to close their hand before seeing it drops and cannot move their hand to help hold. The reaction of their brains that you see is thrown to close their hand long enough that the bill will not take hold.

Save

The pictures with Origami VisitorsWe will not be a financial website responsible if we do not say that savings is one of the many ways. While one dollar may not be seen like a lot, when it is added along with some many dollars passing in your hands each year, they can add quickly in the emergency bag. Send it away into your Piggy bank and keep it on the rain day.

This is clear that a short list of many things can do is actually $ 1, but I hope it contains some things you have never considered before, and breathe your thinking.

Learn more

Here are 17 more important credit than the amount facing your wallet now

The best place to hide the money in your home – negotiations with burglary

Thirty-eight means of making additional money you have never heard

Source link